The biggest question you need to ask yourself when deciding to invest in a Roth 401k or Traditional 401k is do you think your tax bracket is higher today or will be in the future? If it will be higher in the future invest in a Roth 401k if it’s higher now invest in a Traditional 401k.

Whether you invest in a Traditional 401k (before tax) or Roth 401k (after tax), you will still be taxed at your effective income tax rate either going in with the Roth 401k or going out at withdrawal with the Traditional 401k. So the big decision is are you planning to be making less or more money in the future when you want to start withdrawing from your 401k?

No one knows what the tax rate will be in the future, but because you won’t want to use your 401k money until retirement, you might be in a much lower tax bracket when you actually do retire, but who knows?

This is why in my opinion a Roth 401k will make you richer than a Traditional 401k. It’s all about control – since you put the money in a Roth 401k after you’ve paid taxes on it, it can grow tax-free and gives you more flexibility because the gains aren’t taxed when you withdrawal.

While not all companies offer a Roth 401k option, more companies are adding this newer investment option everyday. According recent Vanguard data on Roth 401k plan participation 60% of the companies using Vanguard offer a Roth option, but only 15% of participants choose it.

You should check with your company and strongly consider investing in a Roth over a traditional 401K if you have one available. A Roth 401k will likely make you richer than a traditional 401k and is one of the best investment decisions you can make as a younger investor in your 20’s or 30’s because of the tax-free withdrawal advantages given an uncertain future.

Why a Roth 401k is the Best 401k Investment Choice

Roth 401k’s compound over time and grow tax-free. You pay tax when you put the money in, but not when you take it out likely many years later. This means that all of the compound interest – or money that your money makes won’t be taxed when you take it out. But because you are putting the money in after you’ve paid tax on it you don’t get the benefit of the tax-free savings going in, but you do get it when taking the money out. But this also means you only pay tax on the initial principal (the money you put it), but NOT the gains. Tax-free gains are the real advantage of the Roth 401k.

But what about my tax bracket?

If you are in a lower tax bracket (32% and below) then a Roth 401K is a no-brainer. If you are in a higher tax bracket today it’s a little more complicated, but as a young investor it likely still makes more sense to invest in a Roth 401k instead of a traditional 401k.

Even if you are in your 20’s or 30’s and making a lot of money, this just means you have to pay a higher percentage tax when putting money into a Roth 401k, but still get the advantages of tax-free withdrawals in the future.

Remember this is tax you are paying just on the principal (the money you are putting into a Roth 401k), but the gains will be tax-free. This is where the advantage is – because your gains will likely compound significantly more than the 10-15% that you paid when putting in money if you are in a higher tax bracket.

This means because your gains continue to compound tax-free you will have made a better investment – and made a lot more than 10-15% return on your money over the longer term.

Also if you are in a high tax bracket today, because you will likely be in a higher tax bracket in the future (as you make more and more money) a Roth 401k with no tax on withdrawals is the still the better choice.

INVESTMENT AND INSURANCE PRODUCTS ARE: NOT A DEPOSIT • NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUEThe Battle: Roth 401k vs. Traditional 401k

Let’s look at two different investment scenarios (low to high tax bracket and high to low tax bracket) to see why a Roth 401k is a better investment choice for a young investor who plans to be taxed at a higher rate in the future.

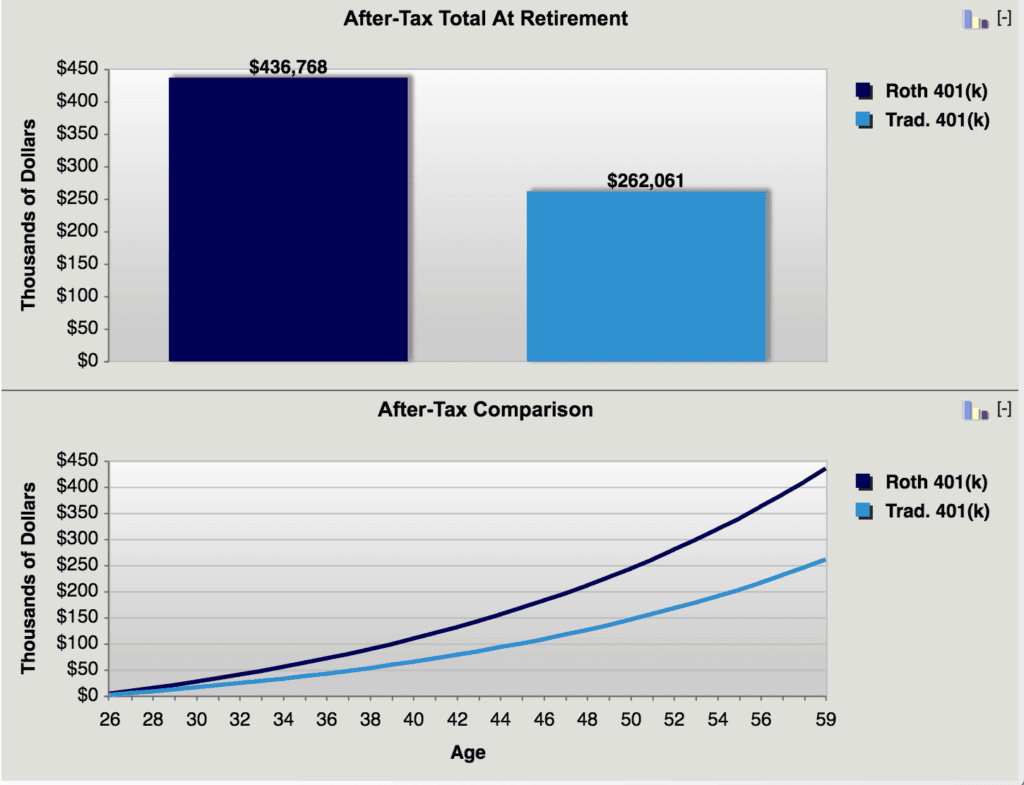

Scenario 1: Low tax bracket now, high tax bracket later (Roth 401k wins!)

Investor age: 26 in 25% tax bracket

Planned retirement age: 65 in 40% tax bracket

Annual 401k contribution: $5,000

Growth rate: 5% annual return

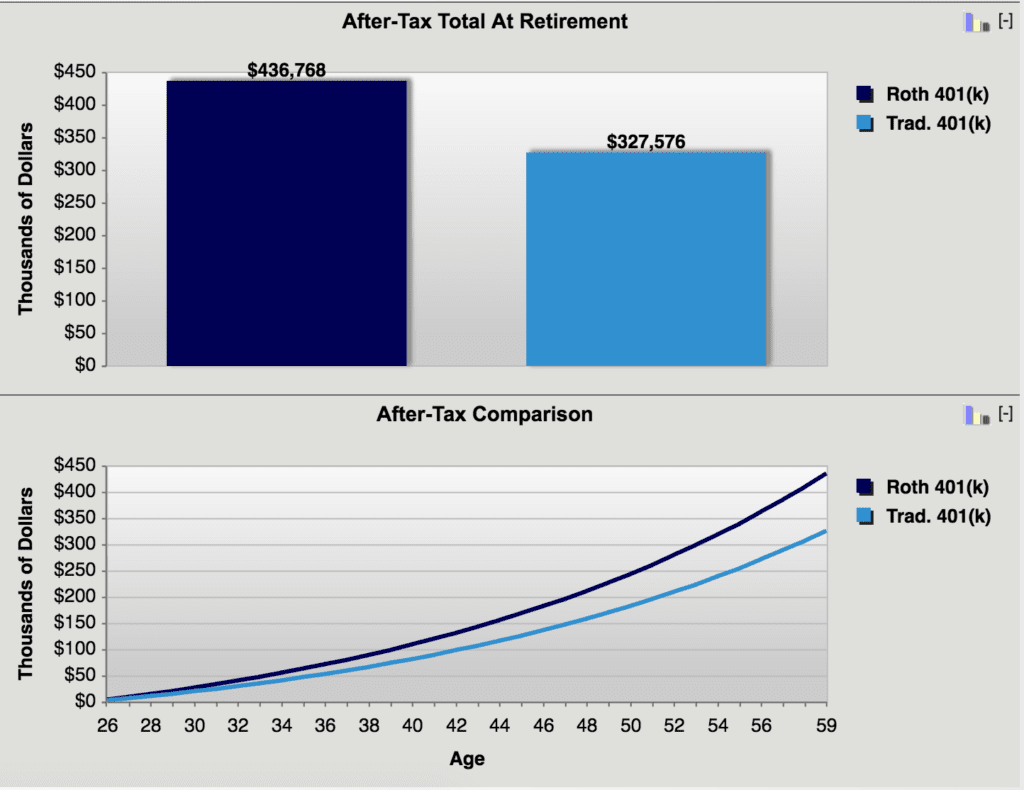

Scenario 2: High tax bracket now, low tax bracket later (Roth 401k wins!)

Investor age: 26 in 40% tax bracket

Planned retirement age: 65 in 25% tax bracket

Annual 401k contribution: $5,000

Growth rate: 5% annual return

How Much Can You Contribute to a 401K?

The contribution limits for a Roth 401k and a Traditional 401K are the same, although you can’t participate in both. Through 2021 you can contribute up to $19,500 per year and a $6,500 catch up contribution if you are over the age of 50 in either a Traditional 401k or Roth 401k. Learn more about the requirements and restrictions of a Roth 401k.

How Much Should You Save in a 401k?

You should invest as much as you can in your 401k, or at least as much as you need to contribute to receive your company match (some companies match your contributions up to a certain percentage of your contribution). If you can max out your 401k it will make you a lot richer in the future than if you don’t. Whether you ultimately choose to invest your money in a Roth 401k or Traditional 401k it will be worth a lot more tomorrow than it is today. So the big question is will your tax rate be higher or lower in the future?

Did you invest in a Roth 401k? Why or why not?

Read 21 comments or add your own

Read Comments