“It looks like I actually have $29,093 in student loans I didn’t really know about…” my wife says way too early on a Saturday morning. I haven’t even had my first sip of coffee.

“What…..?” I must still be sleeping. “Did you just say….” She stops me before I say anything else. “Yes”. It hits me deep in my stomach – $30,000 more in student debt. I spent 5 years paying off my own debt and I knew that my new wife had some debt (maybe $5,000), but not this much.

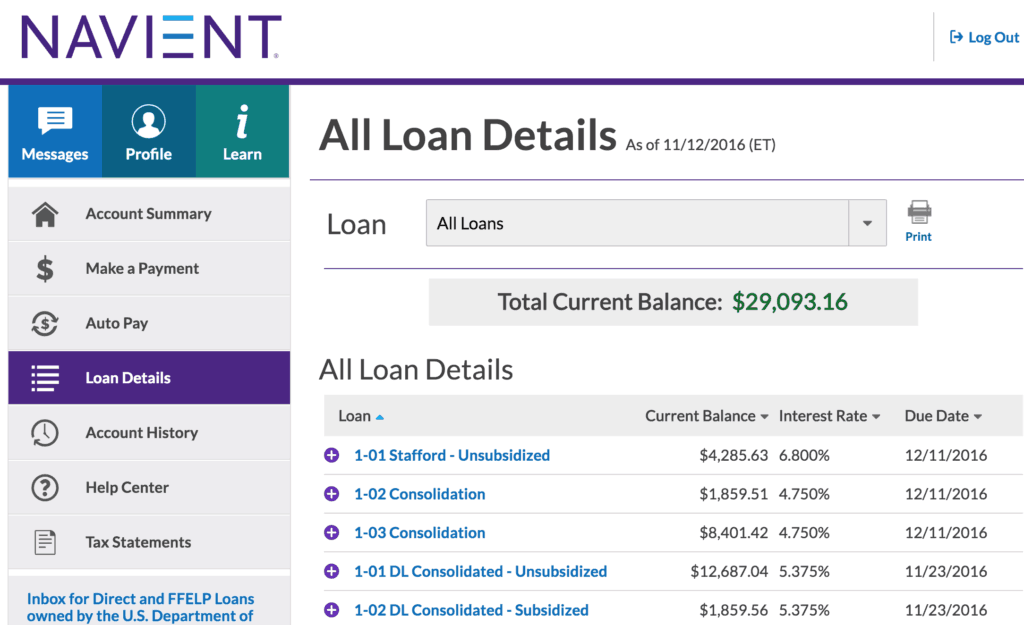

“This has to be a mistake,” I said. She gave me the login to her account and I jumped on my computer. I was awake now and forgot about the coffee. It was true – my wife owes $20,093 in student loan debt – with interest rates between 4.75% and 6.8%. How could this have happened?

How did my new wife have $29,093 in student loan debt that I didn’t know about?

This was my mistake. It might even make the list of my top money mistakes. I knew that I was marrying into student loan debt, but I wrongly assumed I knew how much student loan debt my fiancé had. But the truth is we really only talked about it a few times in passing and I thought she owed approximately $6,000 in student loans – but $29,093 is a different story. That’s more than the down payment I made on my condo.

Why is it hard to talk with my wife about money?

I recently got married in August and up until that point, my wife and I have largely kept our finances separate. While we have had conversations about money before they honestly are tough to have.

The two primary reasons we don’t talk about money are because of the large difference in income between us and my wife just wants me to handle it. She clearly knows how obsessed I am with investing and personal finance, so she trusts I’ll make a relatively good decision when it comes to money.

I have always paid the mortgage and managed all of our expenses, while my wife’s income she uses as her spending money for whatever she wants after contributing to her retirement accounts. It’s worked well for us so we don’t really talk about it. Was this why I didn’t know about her debt?

The mystery of the $29,093 in student loan debt

When I asked her where the student loans came from she said she had no idea. “Seriously???” How can you not know that you owe $29,093 on something? My wife is an incredibly honest person and has never lied to me or intentionally tricked me about money. In fact, some of the qualities that I love most about her are that she’s generous and not greedy about money (very important potential life partner traits!).

So why didn’t she know about the debt? It had to be fraud! I was convinced. Either some kid in Florida took out $29,093 in loans and blew it on Minecraft and Mountain Dew or it’s an organized crime network. I went all Forensic Files on it and started digging into what we did and didn’t know.

It didn’t take long. After a bit of digging we found out that my wife had actually co-signed on student loans with her family, which now were her responsibility! (Note to self: never co-sign anything ever!).

The student loans showed up in her account unexpectedly after more than 10 years. She’s never received a bill for them. She doesn’t even remember signing them. I don’t remember much from when I was 18 either, but still. I let the reality sink in – we went just inherited $29,093 in student loan debt.

Alright, deep breath. I know what’s up. I can crush these student loans like I crushed my own. Marrying into student loan debt doesn’t scare me.

Our strategy to pay off my wife’s student loans

1. Check the StudentLoans.gov website: On this website, I can see if there are any other student loans associated with my wife’s social security number that we don’t know about. This is the easiest way to figure out if someone has fraudulent taken loans out in your name. Although, when I looked up my wife’s loans the information was there, some of it was out of date. It’s definitely worth checking.

2. Request More Information: I am going to call Navient to get the background on all of the loans that have shown up in her account. I am going to request the background paperwork that they have on the loans (since we don’t have it). Ask for as much information as possible and copies of all original loan documents.

3. Refinance the loans: I am going to start shopping the beset student loan refinance companies for rates that are a lot lower than my wife’s current average rate of 5.37%. While I have the cash to pay off her loans completely right now, the simple fact is that I didn’t plan for this unexpected $29,093 expense for the end of this year. I also have other plans for that cash that I am confident will generate a higher return over time than the percentage interest over time.

4. Schedule a regular money convo with my wife: This “new” student loan debt has been a big wake-up call for us. We are both committed to having more focused and productive discussions about money. Neither of us really want to have these conversations, but I am going to push for it even though my wife has no interest in managing our finances. I think it’s important for her to understand the saving and investment decisions I am making for our future.

So what’s next?

Stay tuned to see how I tackle my wife’s unexpected student loan debt over the coming months. And to see how our money conversations go.

Do you have any recommendations for me? What have you done when marrying into student loan debt? How do you have conversations with your partner about money?

Read 15 comments or add your own

Read Comments