Albert Einstein famously referred to compound interest as both the eighth wonder of the world and the most powerful force in the universe.

Yet many investors enter into the stock market without really understanding what it means. They know they should be investing a solid amount of money, and they’ve probably heard that they’re best off if they start early, but many of them are not entirely sure why.

The truth is once you learn the true power of this incredible concept, you’ll want to start investing right away so that compound interest can work on your behalf as quickly as possible.

Compound Interest: A definition

Compound interest is interest that is calculated on the initial principal amount of an investment plus the interest that has already accumulated on a deposit. In other words, compound interest is “interest on interest” that generates over the course of a number of years. The longer the period of time, the higher the amount of interest you’ll rack up.

You can collect compound interest from a variety of deposits and investments, like bank accounts, traditional savings accounts, high-yield savings accounts (HYSA), certificates of deposit (CD), money market accounts, index funds, mutual funds, ETFs, and individual stocks that pay dividends.

Basically, as long as you have an account or fund that promises a return, you will collect interest. And over time, interest will compound and increase your overall pile of money.

Finding the Best Interest Rates

One of the top reasons investors fail to maximize compound interest is because they do not leverage the best interest rates on the market. Sadly, many people are using accounts that have interest rates of between 0.01% and 0.05% APY, or annual percentage yield. In fact, many investors don’t even think to look for higher interest rates.

If more people prioritized this, they’d likely be able to find a financial institution that offers daily compounding interest along with a solid annual percentage rate.

Compare an interest rate of 0.01% APY to an interest account of 0.50% or 0.60% APY, and the difference in compound interest over time can have an astounding impact on your account balance. Granted, HYSAs offer variable rates. But even during downturns, they are still much higher than interest rates offered by traditional banks.

CDs also offer excellent interest rates. They do, however, require you to lock your money for a considerable amount of time (between 3 months to 10 years or more). If you’re looking to invest heavily in CDs, consider using CD ladders, which will give you the flexibility to move money around or roll your funds over into higher performing accounts at various intervals. This can help prevent getting locked into underperforming interest rates that essentially crush the present value of your money.

So, shop around and try to find savings accounts and investment offerings that will give you the combination of the best flexibility to liquidate your money along with the best possible interest rates. This is how you get ahead with compound interest and make a lot of money over time.

How Compound Interest Works

If you are interested in calculating compound interest on your own, there’s a formula for those who enjoy working out math problems on their own.

Compound Interest Formula

A = P (1 + r/n) ^ n*t

In this math problem, A is the total amount you’ll end with. P is your principal contribution (the initial deposit). R is your annual interest rate as a decimal. N is the number of compounding periods per year. And T is the number of years your money compounds.

Tip: Understanding Compounding Periods

Understand that interest can be compounded on different frequency schedules. For example, interest can compound continuously, daily, monthly, and annually.

Make sure to pay close attention to the frequency of compounding when taking out a loan or making a deposit or investment. This will ultimately determine how much you pay or receive over time.

Use a Compound Interest Calculator

If math isn’t your strong suit, there are plenty of free financial calculators available on the internet that you can use to determine the future value of compound interest.

One of the best tools is Investor.gov’s Compound Interest Calculator. Fill out various fields — including initial amount, expected monthly contribution, length of time in years, estimated interest rates, interest rate variance range, and compound schedule — to get a better idea about how much money you could generate over a specific period of time.

You should also consider working with a financial advisor who can help you understand the total value of your investments when you make them. Financial advisors can provide guidance and tips to help you see the long-term value of your investments.

How to Benefit from Compounding Interest

Now that you have a basic understanding of how compounding interest works, it’s time to focus on some ways that you can benefit from this strategy.

To paraphrase the Oracle of Omaha, Warren Buffett, investors should take advantage of compound interest and avoid getting captivated by the siren song of the market. Time is your friend, Buffett says, and impulse is your enemy.

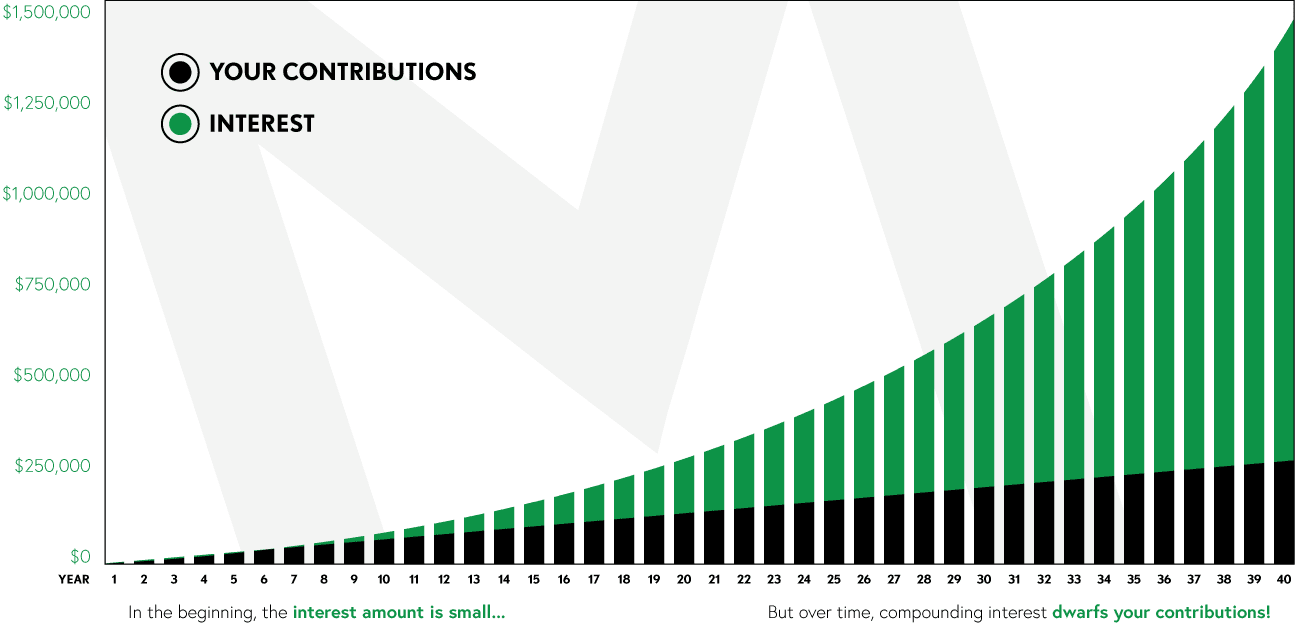

Part of the reason collecting compound interest is so difficult for early investors is because interest takes a significant amount of time to accrue. It can take a decade or longer for interest to compile and significantly surpass the initial investment. But over the course of 20 to 30 years, interest can compile to the point where it dwarfs the initial investment.

The Power of Compounding

Is there anything better than making money off of your own money?

Understanding the Rule of 72

The Rule of 72 is one strategy you can use to determine how long an investment will take to double. This can be applied to investments that have a fixed annual rate of interest.

To calculate the Rule of 72, all you have to do is divide 72 by the annual rate of return.

So, if you have $1 invested with an annual fixed interest rate of 20%, it would take 3.6 years for the investment to reach $2. If the interest rate is 10%, then it would take 7.2 years to reach $2.

Feel free to substitute numbers in the above example as you begin considering your next investment.

Avoiding Credit Card Compound Interest

Here’s the catch about compound interest: It can help you, but it can also bite you.

If you’re not careful about taking out loans from lenders and using credit cards, compound interest can work against you just as much as it can benefit you.

This is frightening when considering that 124 million Americans are in credit card debt, with no sign of this trend reversing any time soon. Many Americans are in way over their heads because they didn’t understand how compounding interest works when they opened a credit account. And now they’re paying for it.

So, be very cautious about collecting credit card debt. Always try to pay off your credit card balance at the end of every cycle to avoid accruing compounding interest. If you have any outstanding payments, it’s in your best interest to pay them down as quickly as possible. Otherwise, the accumulated interest could compound to a point where the total amount snowballs out of control and you’re stuck having to consolidate loans just to make your monthly payment.

Do Student Loans Have Compound Interest?

Student loans have a bad reputation as being unfair to investors. However, people are often surprised to learn that student loans typically use simple interest instead of compound interest. In fact, all federal student loans are required to be simple in nature.

Here’s the difference: Simple loans charge interest on the principal amount only, while compound interest includes interest on the principal as well as unpaid interest that has accrued.

This benefits borrowers because a loan with compound interest is more expensive than a loan with simple interest. Of course, there are some student loans that offer compound interest but the vast majority are simple.

FAQs

How does an annual percentage yield work?

Annual percentage yield (APY) refers to the actual rate of return that will be earned over the course of a year after interest is compounded.

Compounded interest from an APY gets tacked onto a total investment, increasing the overall balance in your bank account or investment portfolio. As such, it’s important to always choose accounts that offer the strongest possible interest rates.

What if my account doesn’t offer interest payments?

If the account you are using doesn’t offer a relatively high rate of interest, then you should strongly consider the purpose of that account. It might be time to look into a better offering with a higher rate of return.

Only you can make this decision. But the whole point of saving and investing is to grow your money. If an account doesn’t offer you interest, or if it offers very low interest, you could be cheating yourself out of a significant amount of income over time.

What is the average rate of return for APY?

The average stock market rate of return is about 10% annually. This has been the case for about 100 years. As such, the stock market is an excellent vehicle for investing and generating a healthy return on your investment.

That said, if you’re considering using the stock market to invest, then you need to be aware of market volatility. Most successful investors will tell you to avoid moving money around frequently and instead focus on playing the long-term game.

Look into index funds and exchange-traded funds (ETFs). That way, you can spread your investments around over a broader area for ready-made diversification, flattening out the effects of the ups and downs of the market a bit.

Can I double my money in the second year of an investment?

You can technically double your money in the first year or the second year of an investment. But you would need an exorbitantly high-interest rate. It’s not impossible to do this. But if you try, it will likely pull you into dangerous waters because you will need to look for fringe investment opportunities that offer much higher return potential, along with higher risks.

Remember to always consider the rule of 72 when investing, which tells you how long you can expect to double your initial investment. Many investors will tell you to get rich slowly by investing in secure or conservative stocks that offer moderate returns over time.

If an investment seems too good to be true, it probably is. But only you can determine this.

Can compound interest lead to exponential growth?

Compound interest is the way to exponential growth when investing or depositing money.

This strategy requires significant patience and being smart about where you park your capital. If you make the right decisions, you can expect to achieve exponential growth over the course of around 20 to 30 years. So, if you’re just entering into the workforce, you can expect to receive the full benefits of compound interest as you approach your golden years — right around the time of your retirement.

Frequent compounding can help you grow your money well beyond your initial investment. That’s why many investors love it.

Can money market accounts offer compound interest?

Some money market accounts offer competitive interest rates which are comparable to high-yield savings accounts (HYSA). However, some can also be very stingy in what they offer to consumers. If you’re considering leveraging a money market account, look around for an account that offers you the best possible rate.

The Bottom Line

As you can see, compound interest is a very powerful concept that can make or break your overall portfolio over the course of several decades.

Investors that choose to pay close attention to maximizing compound interest and minimizing bad compound interest tend to perform much better when it comes to achieving their overall personal finance goals.

Ultimately, the small decisions you make on a daily basis — like putting a few extra dollars in savings, paying down or avoiding credit card debt, and investing in the stock market, will yield massive returns over time. It’s not always possible to see the bigger picture during daily life, which is why investors run into trouble.

Remember: Time is the most powerful tool of all in investing. Make smart decisions and let time do the trick and you are almost guaranteed to wind up on top in the end. Whatever you decide to do, I’ll be cheering you on.

No comments yet. Add your own