Your credit reports – yes, there’s more than one – contain some of the most important information about you.

These reports are available to people and organizations that have a significant impact on your life, including lenders, employers, landlords, and even insurance companies.

For that reason, you’ll need to stay on top of your three credit reports – one issued by each of the three major credit bureaus.

In this guide, I’m going to give a detailed explanation of the three credit reporting agencies. You need to review and monitor your credit regularly, but you should also know who is issuing both the credit reports and credit scores.

Most people are aware that credit bureaus exist. But exactly what they do and how they go about it, is somewhat of a mystery. That’s what I’m going to attempt to unravel here.

Who Are The 3 Major Credit Bureaus?

The three main credit reporting agencies are Experian, Equifax, and TransUnion.

These three are by far the largest credit bureaus in the industry, primarily because they serve as general credit repositories. That is, they maintain credit files and aggregate information on a regular basis on nearly the entire adult population of the United States, as well as people in other countries and even many businesses.

Are There More Than Three Credit Bureaus?

Other agencies may loosely be referred to as credit bureaus, but they serve very specific purposes. In fact, they’re generally so narrow in scope that they tend to operate out of sight of the typical consumer.

For example, Dun & Bradstreet maintains credit databases primarily on large business organizations. ChexSystems serves the banking industry, aggregating information on consumer bank account histories. This information is used by banks to determine if a consumer is eligible to open an account.

But for practical purposes, and for the average consumer, Experian, Equifax, and TransUnion are what is typically meant by the term “credit bureaus.”

What’s On Your 3 Credit Reports?

Each of the three credit bureaus provides a lot more than your credit information. They aggregate data about you from a multitude of sources and include it in their reports.

Typical information you can expect to find on a credit report includes the following:

Personal Information

Any identifying information that either is or has been associated with you in the past will be listed.

Here is some of the personal information found on credit reports:

- Different variations of your name (including your maiden name, previous married names, your name with and without your middle name or initial, or even any aliases you may have operated under)

- Your current and previous addresses

- Your Social Security number

- Birthdate

- Current and former employer information, though this information may not be completely comprehensive

Credit Information

Your credit information is the most significant information reported on each of your credit reports and naturally takes up the largest amount of space.

The types of credit included are:

- Home Financing

- Auto Loans

- Student Loans

- Personal Loans

- Other Installment Loans

- Credit Cards

What it won’t report are your payments to non-credit sources, such as your rent history, insurance premiums, utility payments, and various subscriptions, like gym memberships. However, that second group of vendors may report if you have a charge-off or a collection.

Information about each creditor listed in this section will include the following:

- Name and address of the creditor

- The account number of the loan or credit line

- The date the account was opened

- Account status – open, closed, paid, transferred, in collections, or some other description

- Type of account (credit card, auto loan, etc.)

- Account ownership, which can be individual, joint, or authorized user

- The original amount of the loan, or the maximum credit limit

- The current outstanding balance and monthly payment

- Payment history

Inquiries

Each time your credit report is pulled by a third-party, an inquiry will show up on your credit report.

It will represent confirmation that the information in your report has been accessed. That will undoubtedly happen any time you apply for credit, but it’s also common when you apply for employment, an insurance policy, or to rent an apartment.

Inquiries will generally remain on your credit report for up to two years, then disappear.

When you pull and review your credit report, never ignore this section. You should be familiar with any third party that has accessed your credit report in the recent past. And if you’re not, someone may have accessed your credit report fraudulently.

Public Records

This is probably the scariest part of your credit report, at least it will be if any information appears in this section. That’s because the public records section includes information that’s gone through the court system and has become a legal obligation or event.

Examples of entries that may appear in the public records section include:

- Bankruptcies

- Foreclosures

- Judgments

- Garnishments

- Tax liens

- Liens attached to any real estate you own

The legal information contained in this section will be civil. It will not include criminal records or even motor vehicle violations.

Where Do The Credit Bureaus Get Your Information From?

Let’s start with the credit information since it’s the most abundant. This information is supplied directly to the credit bureaus by the creditors themselves. They’re not required to report your payment history, and frequently will report the information to only one or two of the bureaus, and not all three.

Why would they report the information if they’re not required to do so?

It’s something of a quid pro quo. Since creditors rely on your credit history to make lending decisions, they want the most accurate information available. The only way that happens is when lenders faithfully report to the bureaus.

Each creditor has a vested interest in reporting your information to the bureaus. Because most creditors do, the credit information contained in credit reports is quite comprehensive.

Personal information and public records are derived from several agencies that track that data. And of course, information on inquiries comes from the credit bureaus themselves. After all, each time your credit report is pulled, the respective credit bureau is aware of the inquiry.

How Do Credit Bureaus Calculate Credit Scores?

We’re not going to go too deeply into this topic because it’s a story all its own.

Instead, I’m going to restrict this discussion to a high-altitude view of how the process works.

How Is Your FICO Score Calculated?

There are different credit scores issued, but the official score is your FICO score, which you’ve probably heard of many times.

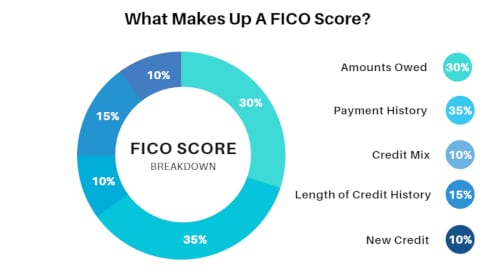

According to myFICO.com, which is provided by the company that created the FICO score model, your score is broken down into five factors.

According to myFICO.com, which is provided by the company that created the FICO score model, your score is broken down into five factors.

Here is the general formula:

- Amounts Owed: 30%

- Payment History: 35%

- Credit Mix: 10%

- Length of Credit History: 15%

- New Credit: 10%

It can be somewhat surprising to see that while payment history is the single largest component in determining your FICO score, other factors make up 65% of the calculation. Your score isn’t determined by your payment history alone.

Notice the 30% comes under the category of “Amounts Owed.” This factor has two components:

Other Factors That Affect Credit Score

The length of credit history represents 15% of your score. Simply put, the longer you have credit established, the greater the positive impact it will have on your score.

New credit is 10% and can weigh your score down if you have too much of it. Since there’s only limited credit experience on these accounts, FICO considers them in a negative light and lowers your score accordingly. You should minimize new credit to improve this factor.

Finally, the credit mix factor is 10%. Though this isn’t too significant, the scoring model considers the types of credit you have. They like to see a good mix between installment loans and revolving lines of credit. For example, if you have five credit lines, and all are revolving, that will weigh against you. But if you have three revolving lines and two installment loans, that will weigh in your favor. Having a mortgage in the mix will also have a major positive affect.

Where Can You Get a Copy of Your Credit Report?

Under federal law, you’re entitled to receive one free copy of your credit report from each of the three credit bureaus each year. Look under the FAQ section below to get contact information for each of the bureaus.

An easier way to get all three reports, that’s also completely free, is to do it through a site known as AnnualCreditReport.com. It’s the only site officially authorized to provide copies of your credit reports from each of the three credit bureaus.

While you should get a copy of each of the three credit reports each year to make sure you have the most accurate information, be aware that they will not include your credit score.

If you’re interested in getting your credit score, you’ll need to consider alternative sources. And fortunately, there are plenty that will provide your credit scores free of charge.

Get A Free Credit Score

Start with your bank or credit union. Most now offer monthly credit scores as a free service. These tend to be more accurate than other free sources because they represent your actual FICO scores, the kind used by lenders.

You can also use free credit score providers. I recommend Credit Karma. You won’t get your official FICO scores, but instead what’s known as VantageScores. These are informational scores, which is to say they parallel FICO, but they aren’t exact or official.

Still, they’re an excellent way to monitor your credit score for free on an ongoing basis. Significant changes in your score can indicate a problem, such as an error or recent delinquency. This will give you an opportunity to deal with those problems immediately.

Monitoring your credit score regularly is an excellent way to track your credit with a regularly updated numeric representation.

Dispute Errors on Your Credit Reports

You should order a copy of your official credit report from all three credit bureaus once a year, at a minimum. But you should also regularly monitor your credit scores. Significant declines, like 30 or more points in one month, can be an indication of derogatory information.

If you know the source of the derogatory information, such as a late payment, there’s not much you can do. But if you have a substantial decline in your credit score, and haven’t made any late payments, there’s a strong likelihood that information has been reported in error.

These can include a creditor reporting a late payment that wasn’t late, the appearance of a collection account that isn’t yours, or – in a worst-case scenario – fraudulent use of your credit.

If any of these events are the source of the credit score decline, you’ll need to move quickly to dispute and correct the errors.

How To Dispute Credit Report Errors

You can dispute a credit entry either by contacting the creditor directly or by disputing the entry with each of the credit bureaus reporting it. If you go through the credit bureaus, they’ll have 30 days to investigate your claim. If the creditor is unable to substantiate the error, the credit bureau must remove it from the credit report.

Federal law is on your side in this case, requiring the credit bureaus to investigate disputes, and to remove them if they are in error.

If you’re going to attempt to resolve the error by contacting the creditor, it’s best to do it in writing. You may need to first contact them by phone to get the name of a responsible party. But everything after that should be done in writing.

Start by getting documentation together. When it comes to either creditors or the credit bureaus, they will usually remove negative information from your credit report based solely on your explanation. But if you can support your claims with documentation, you’re the much stronger case. For example, if a late payment shows up on your credit report, you may need to gather copies of canceled checks to prove that a late payment never happened.

Send a well-worded letter to the creditor describing the disputed information, explaining why it’s in error, and include copies of your supporting documentation.

If the creditor agrees that the entry is a mistake, be sure to get a letter or email from them confirming the error, and agree to contact each of the credit bureaus with the correct information.

Should the creditor failed to report the corrected information to the credit bureaus, you’ll have the creditor’s letter as evidence when you contact the credit bureaus to have the information corrected directly.

FAQ: What You Want To Know About The 3 Credit Bureaus

Here are answers to some of the most frequently asked questions about the three credit bureaus.

Which of the 3 credit bureaus is most important?

There’s really no answer to that question. All three credit bureaus are important because each contains a certain amount of information about you. It’s not possible to say which is the most important, because the three credit reporting agencies collectively provide a virtually comprehensive view of both your credit history and your personal information. Many lenders, particularly mortgage lenders, rely on all three credit bureaus.

The reason they are equally important is because not all creditors report to all three credit reporting agencies. For example, a creditor may report to Experian and TransUnion, but not to Equifax. This is very common across the lending spectrum, so each credit bureau is important in its own right.

Which credit bureau is used most?

Experian is the largest of the three credit reporting agencies, collecting information on more than 1 billion people and businesses worldwide. For that reason, they’re likely the most used of the three credit bureaus.

Equifax is the next largest of the three credit bureaus, tracking information on more than 800 million consumers and nearly 90 million businesses worldwide. TransUnion is a distant third, compiling information on about 200 million people, primarily in the US. It is likely in the least used among the three.

How do I contact the three major credit bureaus?

You can contact each of the three credit bureaus by phone or by email. But be warned by contacting by phone is notoriously difficult. In most cases, you’ll be better off contacting any of the three bureaus by email through their websites.

The contact information for the three credit reporting agencies are as follows:

- Experian: (888) 397-3742

- TransUnion: (800) 909-8872

- Equifax: (800) 685-1111

Understanding The 3 Major Credit Bureaus

Hopefully, the three credit bureaus are less of a mystery now than they were before you began reading through this guide. It’s important to understand who they are and what they do so that you’ll be in a better position to respond to errors and misinformation.

Both your credit and your credit scores are integral parts of who you are in the 21st century. In particular, they have a significant impact on your economic well-being. You owe it to yourself to become familiar with the process and regularly monitor both your credit reports and your credit scores.

No comments yet. Add your own