Every adult needs a financial plan. It’s your roadmap to wealth, guiding you to save money, invest wisely, and prepare for retirement.

So, what is a financial plan? Simply put, it’s a strategy that helps you manage your money to achieve your financial goals. Now, the big question remains: How do you make one? It’s easier than you might think. This blog will break it down for you step by step.

So, stick around to learn the secrets of crafting a solid financial plan that sets you on the path to financial freedom.

What is a Financial Plan?

A financial plan outlines your financial picture, goals, expected milestones, and the strategies and actions required to achieve them.

It considers various factors such as income, expenses, investments, debts, and future financial needs.

Think of a financial plan as a blueprint for your financial success. Just as a well-designed architectural plan ensures a smooth construction process, a carefully crafted financial plan guides you toward a secure financial future.

Benefits of a Financial Plan

Having a financial plan is crucial for several reasons:

- Goal clarity: A financial plan helps you define your short-term and long-term financial goals. Whether buying a house, saving for retirement, or starting a business, a well-defined plan provides clarity and direction.

- Financial stability: A financial plan helps you build a solid foundation for your financial stability. By analyzing your income, expenses, and debts, you can identify areas where you need to make adjustments and take control of your financial situation.

- Risk management: A financial plan includes strategies to manage and minimize financial risks. It considers insurance coverage, emergency funds, and estate planning, ensuring you are prepared for unexpected events. It’ll also factor in the necessary business, auto, health, disability, and life insurance protection you need for your current situation.

- Investment strategy: A financial plan helps you make informed decisions about investing your money. It assesses your risk tolerance, time horizon, and investment options, allowing you to create a tailored investment strategy that aligns with your goals.

- Tax planning: A good financial plan reviews all your liabilities and finds all the available tax deductions.

- Retirement planning: Retirement planning is a key financial plan It helps you determine how much you need to save, what retirement accounts to utilize, and how to optimize your investments to ensure sufficient retirement income to maintain your standard of living.

- Peace of mind: One of the most significant benefits of having a financial plan is the peace of mind it provides. Knowing you have a well-thought-out plan gives you confidence in your financial future and reduces stress about money matters.

A financial plan is essential for achieving financial success. It provides a roadmap to guide your financial decisions, helps you stay organized, and gives you the peace of mind to navigate life’s financial challenges.

By creating and following a financial plan, you can take control of your finances and work towards a secure and prosperous future.

Making a Financial Plan: Step-by-Step

Creating a financial plan is crucial for achieving your financial goals and securing a stable future. It allows you to assess your current situation, set realistic goals, and develop strategies to reach them.

By following these essential steps, you can create a comprehensive financial plan that sets you on the path to financial success.

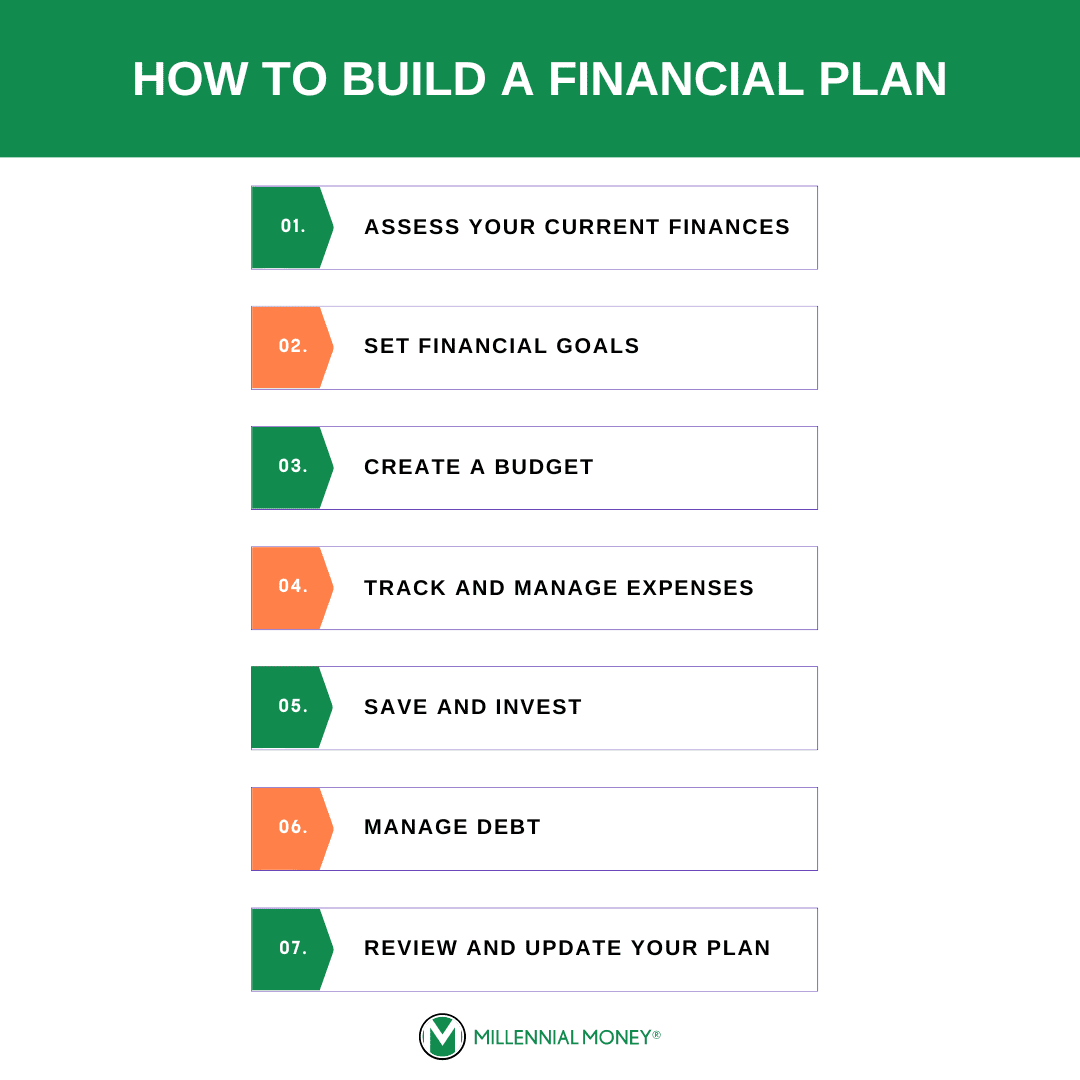

1. Assess Your Current Financial Situation

Before you embark on any financial planning journey, it’s important to understand your current financial situation clearly.

Start by gathering all relevant financial documents, such as bank statements, investment account statements, and credit card statements. Take note of your income, expenses, debts, and assets.

Once you have a complete picture of your finances, analyze your spending habits, debt levels, and savings plan. Consider factors like your income stability, job security, and any financial risks you may face. This assessment will provide you with a baseline for setting realistic financial goals.

2. Set Financial Goals

Setting clear financial goals is a vital step in creating a financial plan. These goals will serve as the foundation for your plan and give you something tangible to work towards. When setting goals, consider both short-term goals and long-term plans.

Building an emergency fund, paying off credit card debt, and saving for a vacation fall into this category, while saving for retirement, buying a house, or paying for college are long-term goals.

Make sure your goals are specific, measurable, attainable, relevant, and time-bound (SMART goals).

3. Create a Budget

A budget is a valuable money management tool. It helps you direct your paycheck towards necessary expenses, savings goals, and investments while ensuring that you live within your means.

Start by writing out your monthly income and fixed expenses to build your budget.

Next, identify variable expenses such as groceries, entertainment, and transportation. Track your spending for a few months to understand your discretionary expenses and cash flow. This process will help you identify areas where you can cut back and save more.

4. Track and Manage Your Expenses

Tracking and managing your expenses is essential for staying on top of your financial plan. Use budgeting apps or spreadsheets to record and categorize your daily expenses accordingly.

Regularly review your spending patterns to identify areas where you may be overspending.

When managing your expenses, consider ways to reduce costs and save money. Consider negotiating better deals on bills, cutting unnecessary subscriptions, and shopping around for the best prices. Small changes can add up over time and contribute to your financial well-being.

5. Save and Invest

Building savings and investments is a crucial aspect of financial planning.

Start by establishing an emergency fund with enough to cover at least three to six months’ worth of living expenses. Once you have an emergency fund, focus on long-term savings and investments. You’ll want to explore high-yield savings accounts so your money can keep up with the inflation rate at a minimum.

Consider contributing to a retirement account, such as an IRA or 401(k), to save for your future. Additionally, explore other investment options like stocks, bonds, mutual funds, or real estate, depending on your risk tolerance and financial goals.

Regularly contribute to your savings and investment accounts to maximize their growth potential.

6. Manage Debt

Managing debt is an integral part of any financial plan. Start by understanding your debt types, such as credit card debt, student loans, or mortgages. Evaluate the interest rates, terms, and repayment options for each debt.

Develop a debt repayment strategy to pay off what’s out systematically. Consider debt management strategies like the snowball or avalanche methods to prioritize and tackle your debts effectively. Make consistent payments and avoid taking on new debt whenever possible.

7. Review and Update Your Plan Regularly

Financial planning is not a one-time activity but an ongoing process. Review and update your financial plan regularly to ensure it remains aligned with your goals and circumstances. Life events, such as marriage, career changes, or growing your family, may require adjustments to your plan.

Regularly reassess your goals, track your progress, and make necessary modifications. Stay informed about changes in tax laws, investment opportunities, and market conditions that may impact your financial plan. By staying proactive and adaptable, you can ensure your financial plan evolves with your changing needs.

Tools and Resources to Help You Make a Financial Plan

The right tools and resources can make a difference when creating a financial plan. The difference between a good financial plan and a bad one is how well you can understand it and thus stick to it. Several options are available, whether you’re just starting out or looking to refine your plan.

Online Budgeting Tools

Budgeting is a fundamental aspect of financial planning. It lets you track your income and expenses and helps you identify areas where you can save and invest. Online budgeting tools have become increasingly popular due to their convenience and user-friendly interfaces.

These tools typically provide features such as expense tracking, goal setting, and customizable spending categories.

Some even offer mobile apps, allowing you to conveniently manage your budget from anywhere and coordinate with other household members. By inputting your financial information, these tools can generate detailed reports and visualizations, giving you a clear picture of your financial situation.

Financial Planning Software

Financial planning software can be a valuable resource for those who prefer a more comprehensive approach to financial planning. This type of software goes beyond budgeting and offers a range of features to help you create and manage your financial plan.

Financial planning software often includes tools for retirement planning, investment analysis, tax optimization, and risk management. These programs typically require you to input your financial data and goals and generate projections and recommendations based on various scenarios.

With the ability to analyze complex financial situations and provide actionable insights, financial planning software can be invaluable for individuals and families looking to optimize their financial plans.

Professional Financial Advisors

While online tools and software can be highly beneficial, sometimes it’s best to seek guidance from a professional. A financial advisor or certified financial planner can provide personalized advice and expertise tailored to your needs and goals.

Financial advisors are licensed professionals with extensive training and a deep understanding of financial strategies.

They can help you develop a comprehensive financial plan, provide investment recommendations, and offer retirement planning, tax optimization, and risk management guidance.

Working with a financial advisor can provide peace of mind, knowing that you have a trusted expert guiding you through the complexities of financial planning. They can help you navigate challenging financial decisions and provide ongoing support to keep your plan on track.

When to Create a Financial Plan

Creating a financial plan is crucial in achieving financial security and reaching your long-term goals. Here are some key moments when it’s important to create a financial plan:

- Starting a career: As you begin your professional journey and earn a steady income, laying the foundation for your financial future is essential. Creating a plan at this stage will help you manage your income, set a budget, and start saving for the future. Revisit your financial plan every time you get a new job, promotion, or change in your income.

- Getting married: Marriage brings together two individuals and their finances. Combining your financial goals and aspirations requires careful planning. A financial plan will help you and your spouse align your priorities, plan for joint expenses, manage debt, and build a strong financial future

- Starting a family: Welcoming a child brings joy and added responsibilities. A financial plan becomes crucial as you consider the costs of raising a child, such as education, healthcare, and extracurricular activities. Planning will help you meet your family’s needs and secure their financial well-being.

- Buying a home: Purchasing a home is one of the most significant financial decisions you’ll make. It’s important to create a financial plan before taking this step to evaluate your affordability, understand mortgage options, and plan for associated expenses like property taxes, maintenance, and insurance. A well-thought-out plan will help you make an informed decision and avoid potential financial pitfalls.

- Preparing for retirement: Retirement may seem distant, but it’s never too early to plan for it. Creating a financial plan early on will allow you to determine how much you need to save, explore retirement accounts and brokerage accounts, and choose specific investments to build a nest egg that will support you during your golden years.

- Changing careers: Transitioning to a new career or starting a business can be exciting but also uncertain financially. A financial plan can help you evaluate the financial implications of such a change, including potential changes in income, benefits, and retirement savings. This prep work will enable you to make informed decisions and ensure a smooth transition.

- Experiencing significant life changes: Significant life events, including divorce, the death of a spouse, or inheriting a substantial amount of money, can have a profound impact on your financial situation. During these times, it’s crucial to reassess your financial goals, revise your plan, and make necessary adjustments to ensure your financial well-being.

- Dealing with debt: If you are burdened with debt, creating a financial plan becomes even more critical. A plan will help you develop a debt repayment strategy to pay off debts efficiently, avoid further debt accumulation, and regain control of your financial situation.

Bottom Line

A financial plan is a crucial tool that helps individuals and businesses manage their finances effectively. It provides a roadmap for achieving financial goals, whether saving for retirement, buying a house, or starting a business.

To create a solid financial plan, one must first assess their current financial situation, set realistic and measurable goals, create a budget, and regularly review and adjust their plan.

By following these steps and seeking professional advice when necessary, anyone can take control of their finances and work towards a secure and prosperous future. Remember, a well-crafted financial plan is the key to financial success and peace of mind.

No comments yet. Add your own