If you use a credit card to make daily purchases, MaxRewards might be a great asset to you.

MaxRewards reviews your spending and will recommend the best credit cards with the best offers that will benefit your spending habits.

The app will also provide you with recommendations on cards with no annual fees, daily rewards, and bonus limits. And as an added bonus, if you like cash back, the app will help you save money through earning the best cash back.

About MaxRewards

Travel rewards have traditionally required a lot of time and effort. Anik Khan, MaxRewards’ CEO, knows this first hand. He earned over $20,000 in rewards over the past few years!

However, he spent a significant amount of time and effort in doing so. From a financial standpoint, it was definitely worth it (and he also genuinely enjoys maximizing the system), but he knows most people don’t care for the hassle.

That’s why Anik and his team built MaxRewards. It’s an app that makes reward maximization simple, for novices and experts. He wanted to make his own life easier and share the incredible benefits of reward maximization with the other 99.9% of Americans who weren’t credit card gurus.

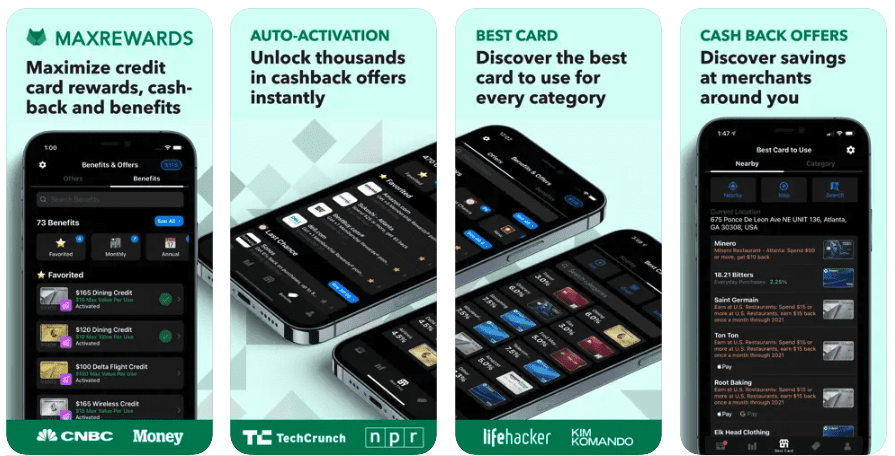

How MaxRewards Works

Connect Your Existing Credit Card Accounts

First, you connect your existing credit card accounts. The app pulls in your historical transactions and estimates how you spend. You can adjust it to reflect your expected future expenses.

Set Your Preferences

Then, you indicate your preferences, like what cards you don’t want. You can also specify if you’re a student or active duty military. That’s actually all the input you need to provide to get your personalized recommendations.

Get Your Personalized Recommendations

I have to say, when I found out how they come up with recommendations, I was blown away. It’s legit next level. The app simulates over a million different scenarios to mathematically find the best combination for you! It factors in:

- Everyday base rewards

- Category bonus rewards

- Revolving category rewards

- Bonus limits

- Sign-up bonus and expected qualification

- Intro and ongoing annual fees

- And so much more

One of the factors I thought was really cool was the ongoing net rewards rate. Essentially, the app excludes cards that are more expensive than it’s worth (i.e. annual fee > rewards).

After you get your recommendations, the app puts everything you need to do in a dynamic action plan. It factors in rules like Chase 5/24, so you should follow the recommendations exactly to maximize your odds of approval (and rewards).

Sign Up Bonus Tracker

Once you open a card, you can use the sign-up bonus tracker to track your progress toward the bonus. Once, I was a few dollars short of getting a sign-up bonus worth $1,000+. I called the issuer a few days after the deadline, and they would not budge, even though I had spent thousands more on the card already. I was pissed! I wish I had MaxRewards then.

Best Card To Use Feature

After you’ve opened all of the recommended cards, you can use the “Best Card to Use” feature to maximize your earned rewards from every transaction. The app accounts for all the nuances like revolving categories, bonus limits, and point valuations so you don’t have to.

Finally, MaxRewards shows your spending, rewards, and credit scores from all of your accounts. There are several apps that pull in your spend, but this is the only app I’ve seen that also pulls in rewards and shows you the expected dollar value of all of your points, miles, etc. I also like how I see a different credit score for every connected bank.

Fun Fact: the team at MaxRewards actually built their own integrations with issuers so that they could pull in all of this data.

Overall, I really like how MaxRewards works. You don’t need to make any confusing choices like “reward cards vs. travel cards,” you get personalized, objective recommendations in minutes, and you don’t even need to keep up with sign-up bonuses and revolving category bonuses.

I also love the fact they built their own integrations so you could get rewards, spending, and credit scores in one app.

Fees

Is MaxRewards free? Yes, the app is free to download and use and most of its functionality is free. However, MaxRewards offers a premium plan called MaxRewards Gold, though you can pick your own rate up to $25/month.

What Banks Does MaxRewards Work With?

MaxRewards supports cards from top financial institutions including:

- American Express

- Bank of America

- Barclays

- Capital One

- Chase

- Citi

- Discover

- US Bank

- Wells Fargo

Security

You can rest assured that MaxRewards is keeping your information safe and secure. They use bank-level encryption, never access credit card numbers, or social security numbers and do not sell your data to third parties.

Pros and Cons

Nothing in life is absolutely perfect, and the same goes for MaxRewards, lets cover some of the pros and cons:

Pros:

- Personalized Reward Tracker

- Personalized Sign-Up Bonus Tracker

- Personalized Credit Card Recommendations Based on Spending

Cons:

- Have to pay a fee for the best features

Frequently Asked Questions

Is MaxRewards app safe?

Yes, MaxRewards is safe. They use bank-level encryption, never access credit card numbers, or social security numbers, and do not sell your data to third parties.

Does MaxRewards cost money?

The majority of the functionality on MaxRewards is free, but if you want to be a Gold Member, that will cost you up to $25 per month, but the good part is that you get to set your monthly rate dependent on how much you save each month.

Who Shouldn’t Use MaxRewards?

The team at MaxRewards designed the app to be useful for travel reward beginners, veterans, and everyone in between. But MaxRewards won’t be valuable if you’re paying 20% interest.

In general, if you already have a lot of debt, if you constantly overspend on your credit cards, or if you consistently carry a balance, MaxRewards is probably not for you. If you’re struggling with credit card debt, read

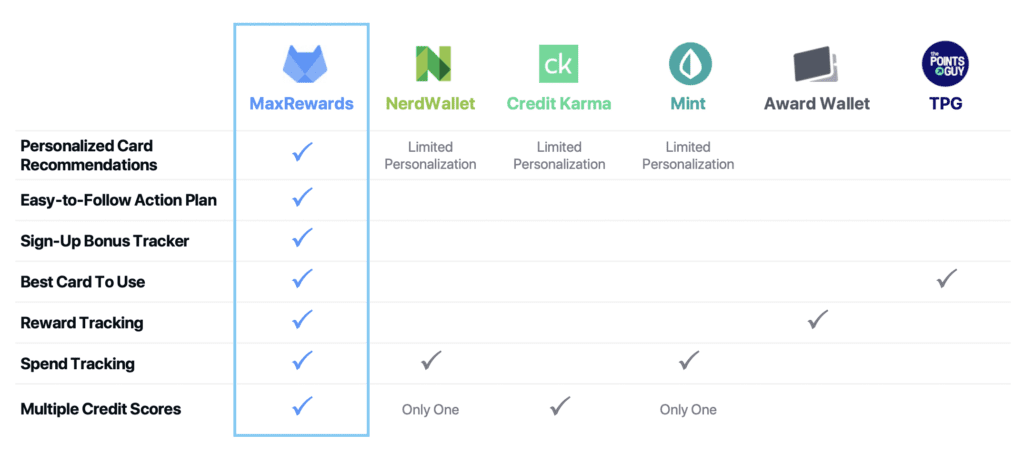

MaxRewards is the Personal Capital for Credit Cards

I really like where MaxRewards is going, and I think it can become the Personal Capital of credit cards. As most people know, I think Personal Capital is the best app, hands down, to track my money and wealth. It’s a complete solution, and I think MaxRewards is the complete solution for credit cards. Here’s how they stack up against other popular personal finance apps:

There’s really no competition. When it comes to credit cards, MaxRewards is the app to get.

What Are Travel Rewards?

Credit card reward maximization is strategically earning and redeeming credit card rewards to get exceptional value. Since some of the most desirable and valuable redemptions are travel-related (e.g. flights, hotels, vacation bundles).

Reward maximization is NOT just getting a new credit card and redeeming the sign-up bonus for a flight. The reward seeker is strategic; she carefully selects the best cards, always earns the sign-up bonus, consistently uses the best card for each merchant and brilliantly redeems her rewards for maximum value.

For her effort, she may earn 2-4x more in value than a layperson with the same annual spend. That translates to about $2,000–$3,000 in rewards a year, and that’s just for an average spender.

Credit Card Rewards Are More Valuable Than Money

Those of you who proclaim “Cash is King” might consider the above statement blasphemous. But I bet that you paid tax on almost every source of cash you earned. Credit card rewards are one of the few benefits that are still not taxable. When you redeem your rewards for a trip worth $2,000, it’s like getting a $3,000 bonus pre-tax (the $1,000 goes towards FICA, federal income tax, and state income tax).

Another aspect of rewards that can them more valuable than money is their limited redemption options. Yep, you read that right. Limited redemption options mean that you don’t feel guilty when you book a luxury vacation. Every “real” dollar you splurge on an expense can be saved or invested. Rewards. Not so much, so using them doesn’t come with buyer’s remorse.

Finally, “free” is always better. A $3,000 first-class flight to Europe is nice. Using your rewards to book it–now that’s amazing.

Will Reward Maximization Hurt My Credit?

You may be thinking, “Great! I can vacation in Bali for the low, low cost of busting my credit. ????” That’s one of the biggest misconceptions of reward maximization. If you’re doing it right, you will NOT hurt your credit.

Here’s why: Your credit score is based on several factors. One such factor, which contributes to about 10% of your overall score, is the number of recent credit inquiries. When you apply for a new card, a new inquiry is added to your report. For most people, this will temporarily bring down their credit by a small amount.

However, opening a card will also increase your overall credit limit. This helps your credit utilization, which contributes to a much more meaningful 30% of your score. As you pay off your card every month, you add positive data points to your payment history, which contributes to 35% of your overall score. So for most millennials, who typically have a limited credit history, opening new cards will generally increase their credit score with the BIG, BIG caveat that they’re responsibly using them.

One thing everyone should be clear about: earning rewards by getting into credit card debt is NOT reward maximization. That will definitely hurt your credit.

Read 2 comments or add your own

Read Comments