Mint.com has been one of the most popular money management apps on the market since it was launched in 2006. Since the app’s announced shutdown in January of 2024, you may be wondering what Mint alternatives do you have for keeping track of your finances and building a budget.

We’ve compiled a list of the best Mint alternatives, looking at their features, fees, and customer reviews.

11 Best Mint Alternatives

Here are the best Mint alternatives to help you manage your finances more effectively:

1. Empower (formerly Personal Capital)

🏆 Best Overall

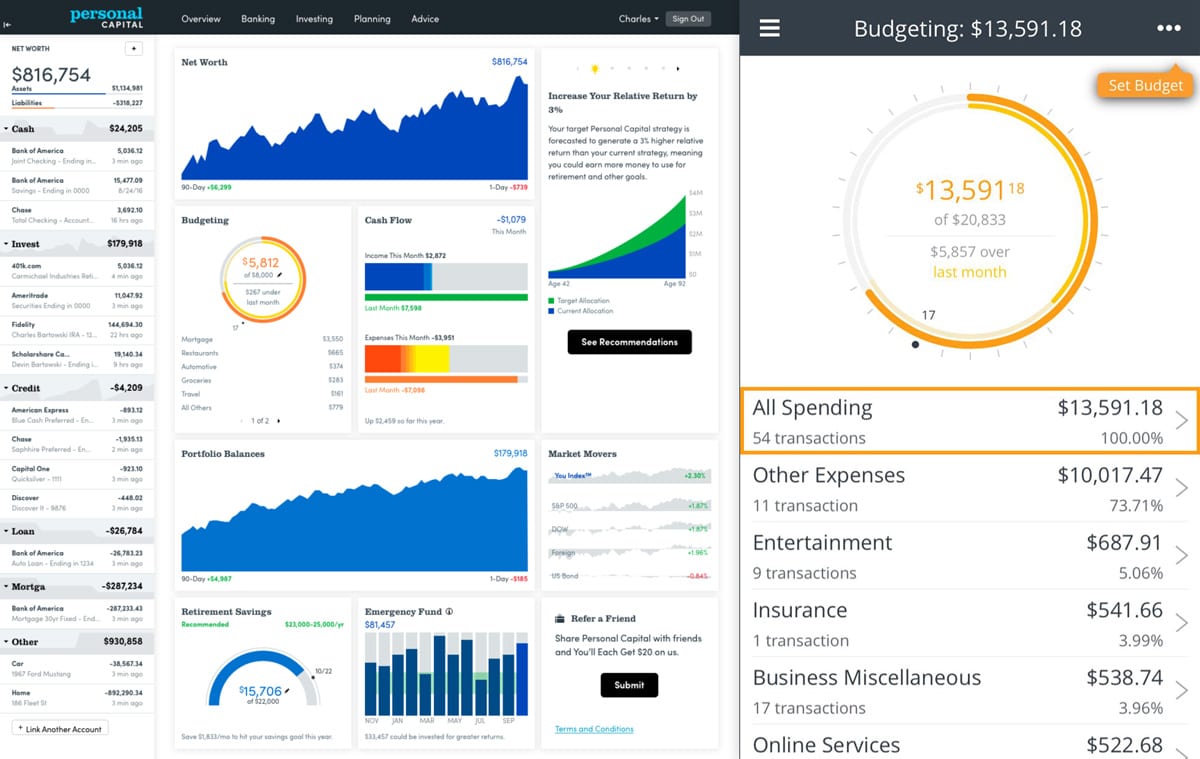

Personal Capital has been around since 2009, but it has gained quite a bit of popularity in the past few years.

Generally speaking, it’s more focused on tracking your net worth and investments, but it also has a budgeting section that offers the same income and expense tracking.

The app allows you to link all of your financial accounts. Then, any time you spend money, your purchases will automatically be categorized in the budgeting section (occasionally this is inaccurate, so you may have to manually change the category on some purchases). This categorization can be as general groups like you see in the screenshot above (“Entertainment”, “Insurance”, etc), or in customizable fields that better work for you.

For any time frame, you can then see which expenses take up what percentage of your personal budget, and what your savings rate is.

PRICING

The software is completely free to use.

Next Steps:

- Track Your Finances Now with Empower

- Read our full Personal Capital Review

2. You Need a Budget (YNAB)

![]()

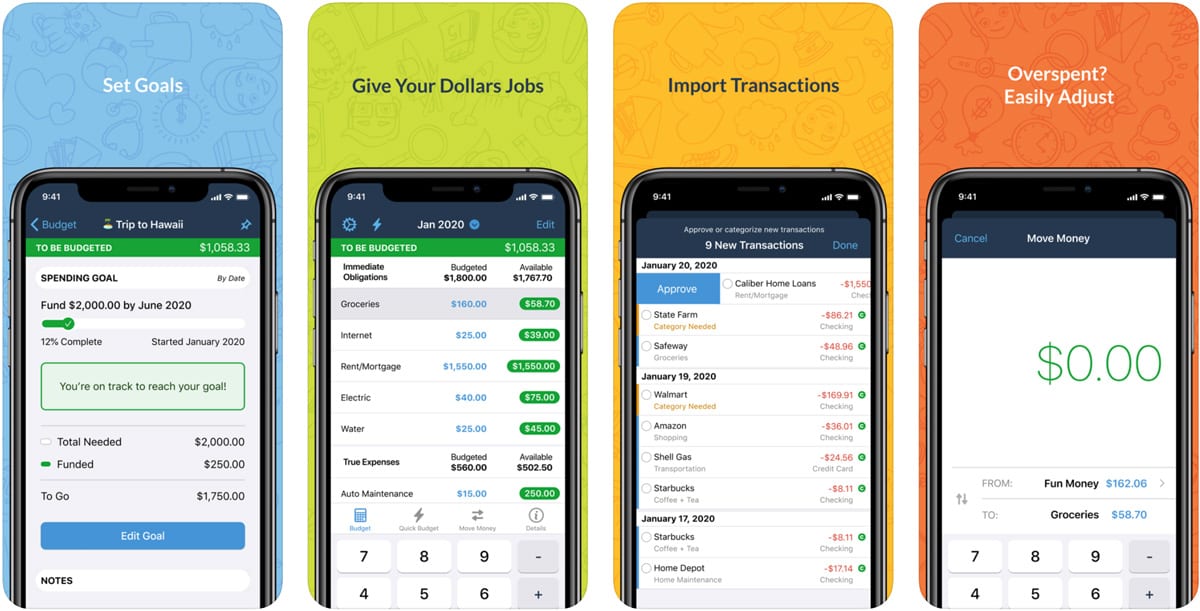

YNAB is solely a budgeting app. It also emphasizes financial education as it looks to make its user into savvy budgeters. The newest version of the YNAB app has a clean interface – something Mint users will appreciate.

In the past, you had to import all of your financial information into YNAB manually. This is no longer the case. In the newer versions, you’re able to log into your bank, credit cards, etc., and automatically import data.

YNAB is generally based on the concept of zero-based budgeting: its #1 rule is to give every dollar a job. Such is the case with zero-based budgeting, where you have no money left over because every dollar is accounted for.

At the same time, it teaches you not to pinch pennies by cutting out expenses you’d prefer to keep.

PRICING

34-day free trial then as little as $7 per month when paid annually.

Next Steps:

3. Quicken

![]()

Quicken is probably the most established personal finance software on this list. If you want to be able to handle your investments, taxes, and budgeting in one app, then you can’t get much better than Quicken.

With the depth of its features, Quicken can be used by someone with a net worth of $10 or $10 million.

In terms of being an alternative to Mint, Quicken lets you view all of your transactions and accounts in a single place, create and manage spending categories, see how much you’ve spent and how much you’ll have left after you pay your bills, set savings goals and more.

You can see transactions by household member, and even pay bills straight from Quicken.

PRICING

30-day free trial then $34.99+ annually.

Next Steps:

4. PocketGuard

![]()

PocketGuard is a simple, mobile-only budgeting app that helps you keep track of your daily spending while also finding new ways to optimize your budget.

Like many of these apps, it works by having you link your checking account, investments, and credit cards to automatically pull in your income and expenses. Once everything is linked, it will automatically pull in all of your transactions and income.

What it does that is slightly different from other apps is its “safe to spend” metrics – how much you can safely spend without going over budget. The app is currently mobile-only, and you can’t contact them by phone.

Still, it’s simple, and the proactive approach makes it worthy of a spot on this list.

PRICING

$4.99 per month or $34.99 annually.

Next Steps:

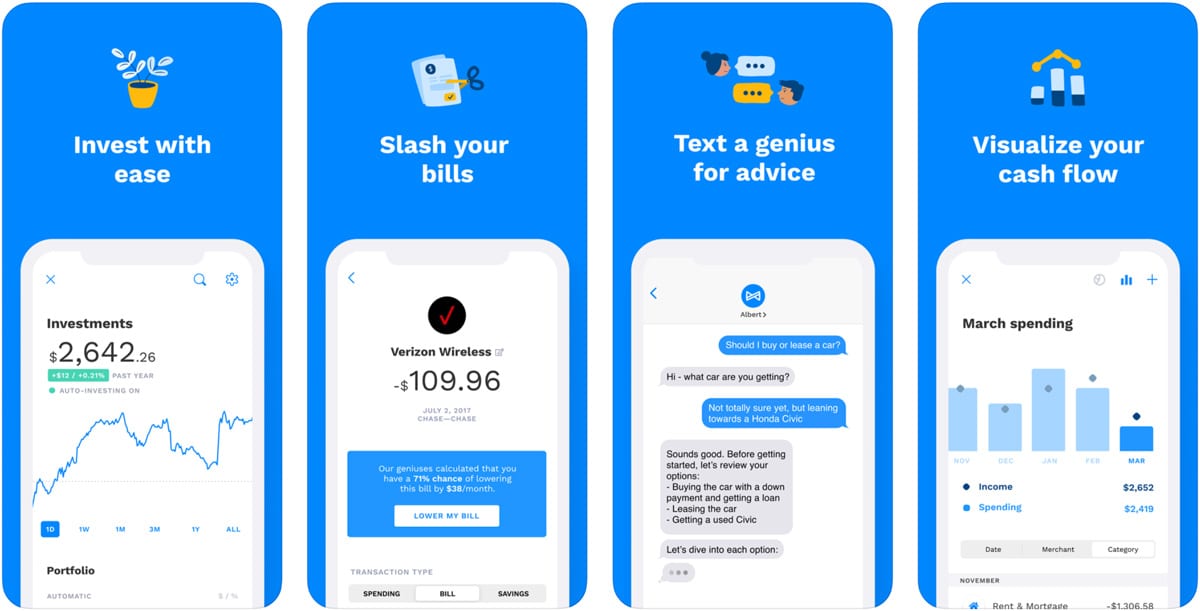

5. Albert

![]()

Like Personal Capital, Albert does a lot more than just budgeting. It helps you transfer cash, invest, set savings goals, and its “Geniuses” will guide you through various financial decisions or alert you if you’re overpaying for anything.

For the free, self-managed app, Albert lets you:

- View all of your accounts in one place, set up a budget, and see how much you have left to spend for the month

- Save automatically, either by a fixed amount or using their “Smart Savings” algorithm which determines how much you can safely save at any given point. The savings account lives in the Albert app, but can be transferred to a different account at any time. Note: They’ll give you a bonus of 0.10% (or 0.25% for Genius subscribers), but you can beat this by a lot with most high-yield savings accounts.

- Works with Billshark to lower your bills. The company boasts that on average, they can help you save up to $250+ per year.

- Access to instant, interest-free cash advances, up to $100.

If you want access to their “geniuses” for guided investing, account monitoring, and an additional bonus to your savings, or financial advice, you will have to pay for it.

Regardless of which you choose, the interface is clean and easy to use and gets high praise from its users (rated 4.6 stars on iOS and 4.0 on Android).

PRICING

Self-manage and core app for free, or Albert Genius for $14.99 per month. When you join Albert, you’ll have a 30-day trial for Albert Genius. If you don’t cancel within 30 days of signing up, you’ll be charged for a subscription, which auto-renews until you cancel it.

Next Steps:

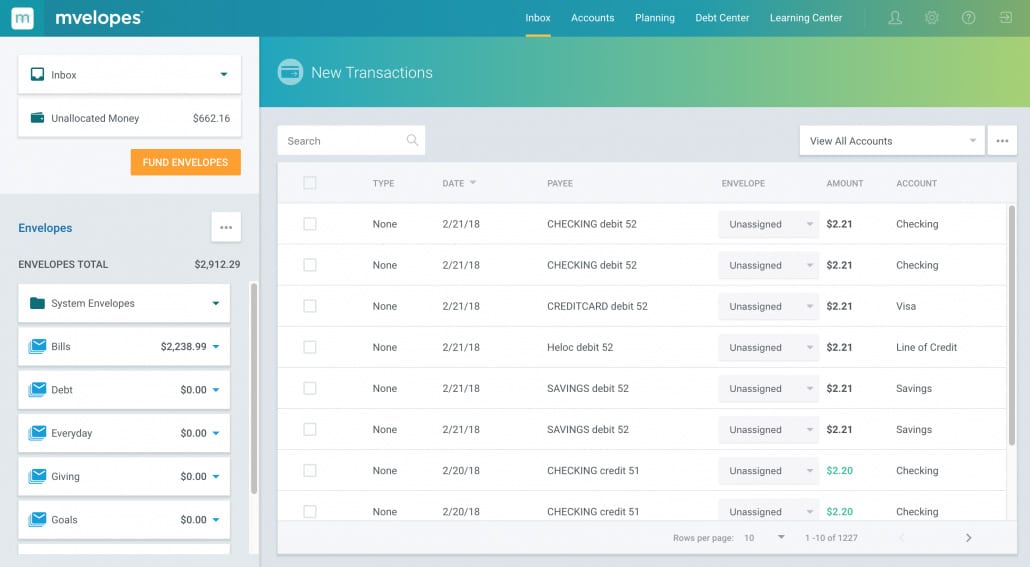

6. Mvelopes

![]()

Mvelopes is a budgeting app based on the budget envelope system. With Mvelopes, you use digital “envelopes” instead of paper ones.

The benefit of doing it digitally is that you can link your financial accounts; thus, you can track your budget categories automatically.

The app has a simple interface and is easy to use. It’s available as a web-based version on your desktop or as an app on your phone. There is, unfortunately, no free option. The fee could be worth it, though – especially if budget envelopes help prevent you from overspending.

PRICING

60-day free trial then $6-$19 per month.

Next Steps:

7. Wally

![]()

Wally is a mobile-only budgeting app that has evolved over the years.

Originally, Wally required a more hands-on approach. You couldn’t link your bank or other accounts, so all transactions had to be entered manually. Some enjoyed that approach and actually preferred it over the others on this list for that very reason.

Today, Wally allows you to sync your accounts and track your spending automatically. One cool feature is that once you sync your accounts, Wally instantly shows you insights on the past 2 years of spending. That means you might find ways to optimize your budget right from the start, instead of waiting until you’ve used the app for a few months.

Wally shows your daily spending and allows you to set savings goals. You set savings targets manually, but the app recommends saving 20% of your income.

You’ll also see your remaining budget, so you immediately know how much you have left to spend.

PRICING

Basic version for free, or premium “Wally Gold” version for $1.99 per month or $24.99 per year. Alternatively, you can opt into individual features of Wally Gold for $5.99-$11 per year.

Next Steps:

8. Money Manager: Budget Planner

The Money Manager Budget Planner app was created by learnings.ai and you won’t find it being mentioned in very many list articles, probably because it hasn’t been around very long. However, it’s rated exceptionally well on the Apple App Store.

In addition to the features most other budget apps have, such as creating graphs and budget categories, you can also set daily reminders to enter your expenses. However, doing so is necessary because you can’t link the app to your bank and credit cards.

Still, the app is free, it creates nice visualizations, and there are no ads to distract you.

PRICING

The app is totally free.

Next Steps:

9. Goodbudget

![]()

Goodbudget is another budget envelope app, but it has some unique features that set it apart. For example, you can sync your budget to multiple devices and share your budget with a partner.

The app creates spending graphs, lets you create customizable spending periods, and allows you to set scheduled transactions and envelope fills. Plus, you’ll see all of your “envelopes” laid out, showing how much you have left in each of them.

PRICING

Basic version for free, or premium version for $7 per month or $60 per year.

Next Steps:

10. Bluecoins Finance

![]()

Bluecoins Finance is a manual expense tracking app, but it does a great job without being overly complicated.

It is great because of how seamless it is. You enter your expenses, and they will immediately be remembered. Plus, it will then be able to autofill expenses you previously loaded into the app.

PRICING

One-time cost of $8

Next Steps:

11. Wallet by BudgetBakers

![]()

Rounding out this list is Wallet from BudgetBakers.

It has a colorful yet simple interface. According to Wallet, the app can sync with over 15,000 banks worldwide. This is a premium feature, however. In the free version, you’re required to manually enter transactions for expense tracking.

This app is seriously feature-packed. You can export your budgets to an Excel file, share your expenses, and generate budget reports to help break it all down, making this a great app.

One insightful feature is the ability to rate your transactions. It can be a good exercise to reflect on your spending and where you can clean up.

PRICING

Basic version for free, or premium version with automatic syncing for $5.99 per month or $21.99 per year.

Next Steps:

Which Mint Alternatives are Best for You?

Many of these top Mint alternatives achieve a lot of the same basic functionality:

- how much you have in your bank account(s)

- credit card balances

- investments, and more

When it comes to look and feel, though, the most similar site is – Empower.

No comments yet. Add your own