In this post I will show you the exact portfolio and allocation strategy I’ve used to beat the S&P 500 and Dow so far this year. I did it without making a single trade or buying a single stock. I didn’t day trade or make any of my previous investing mistakes. In fact, I didn’t do much of anything except let my well-researched mix of index funds that I built in 2014 ride – with a few small tweaks. I like to call this the Millennial Money portfolio – my personal long term passive investing strategy influenced by the coffeehouse lazy portfolio, with my own modifications (mostly more exposure to emerging markets).

I am not an investing professional (but most professionals don’t beat the market over time!) and even though I feel confident in my portfolio allocation and fund selection strategy I welcome feedback – so please share your thoughts or questions in the comments. I am definitely still learning, but this strategy has worked well for me.

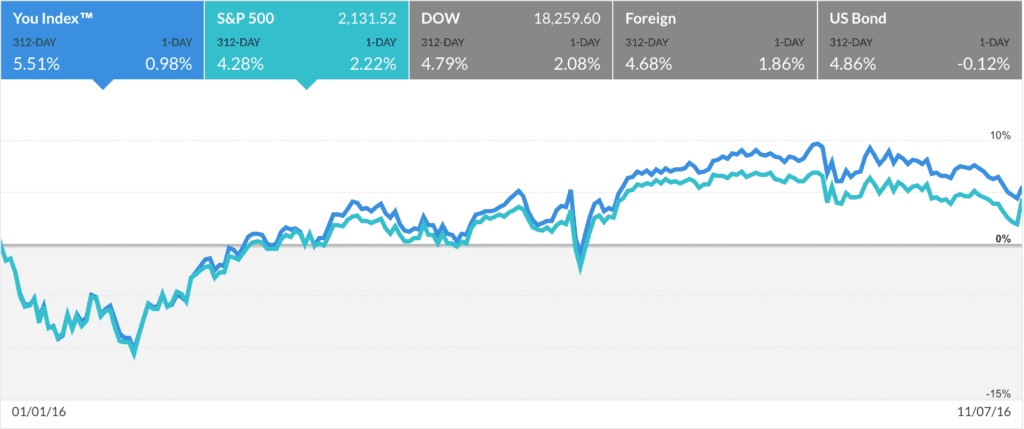

The Millennial Money Portfolio has beat the market by 1.23%

Here is a look at my returns year to date for 2016. Note how my year to date return is 5.51% compared to the S&P 500 4.28% growth and the Dow 4.79% Dow returns. While a return of 1%+ might not seem like a lot, this will compound over time and give me an advantage over the market if I can sustain these gains. One piece of advice – because it’s so easy to use Empower I used to check my portfolio daily or multiple time a day. It drove me crazy so I only check it once a month now.

All of the images below are from the free account that I have at Empower, formerly Personal Capital. They allow you to track all of your investment performance and provide free asset allocation recommendations.

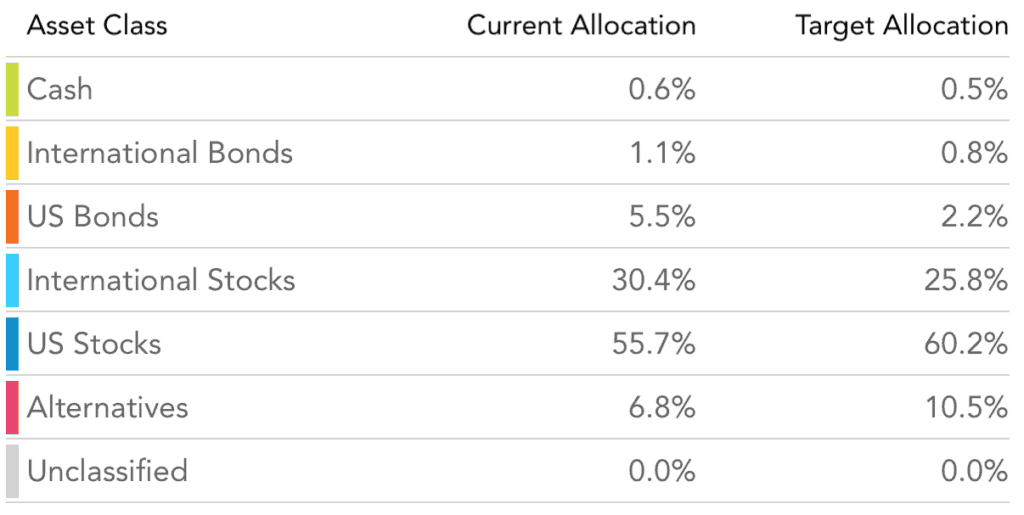

The Millennial Money Portfolio Asset Classes and Allocations

Your investments by asset class and target allocation in many cases matters more than the funds that you select. This represents your exposure to different markets, so it’s important to find an ideal target asset allocation for your age and risk tolerance and try to hit it with your mix of funds.

The following is a breakdown of my exact portfolio by percentage asset class. You can see that I invest in a mixture of domestic and international stocks bonds, as well as alternative investments. I try to keep this percentage allocation very close to my target levels, which does require a bit of re-balancing every now and then.

I usually re-balance my portfolio twice a year or if something super weird happens and it gets more than 5% out of whack. I am planning to re-balance my portfolio on January 1st and you can see that I am getting close to being 5% off due to some strong returns in my international stock holdings over the past few months.

The Millennial Money Long Term Investment Portfolio

The following is a list of the exact funds that make up my portfolio. I chose this mix after a lot of research on Morningstar, the Bogleheads forum, and reading the best books on investing. While I have previously tested platforms like Betterment and reviewed services like Vanguard Personal Advisor Services, I ultimately wanted to the control of building and managing my own investment portfolio. It doesn’t take a lot of work, forces me to learn more about what I am investing in, and gives me more control.

This is by no means a recommendation on what you should invest in – just what has worked well for me over the past few years. I hope it gives you a few new ideas. The following funds I currently hold my longer term investments vehicles, but not all of these funds are in the same investment account. I invest some of these in my tax deferred (Roth 401k and Roth IRA) and others I invest in a taxable account once I have maxed out my pre-tax contributions limits. I use my tax advantaged accounts for funds where more trading occurs to I don’t get taxed on the gains, and only invest in full index funds (VTIAX and VTSAX) in my taxable account since there is little trading volume so I can minimize my tax exposure.

Check out the funds below and build your best mix to hit your ideal asset class allocation.

Cash

VMMXX: Vanguard Prime Money Market Fund

Stocks & Bonds

VWENX: Vanguard Wellington Fund Admiral Shares

International Stocks

VTIAX: Vanguard Total International Stock Index Fund Admiral Shares

VWO: Vanguard FTSE Emerging Markets Index Fund ETF Shares

US Stocks

DVY: iShares Select Dividend ETF

IJR: iShares Core S&P Small-Cap ETF

VO: Vanguard Mid-Cap Index Fund ETF Shares

VTSAX: Vanguard Total Stock Market Index Fund Admiral Shares

VTV: Vanguard Value Index Fund ETF Shares

VUG: Vanguard Growth Index Fund ETF Shares

Alternatives

What do you invest in?

Read 23 comments or add your own

Read Comments