With no minimum balance, affordable fees, and an advanced yet user-friendly platform, Betterment has removed a lot of the barriers to investing.

I’m not surprised the service has emerged as a consistent leader — especially among millennials — in the fast-changing world of robo-advising.

But new robo-advisors start up all the time. Before joining the 700,00+ people with assets managed by Betterment, let’s take a closer look at how the service works.

What Is Betterment?

Betterment is a robo-advisor, which means the service uses a computer algorithm instead of a human broker to invest your money and rebalance your portfolio.

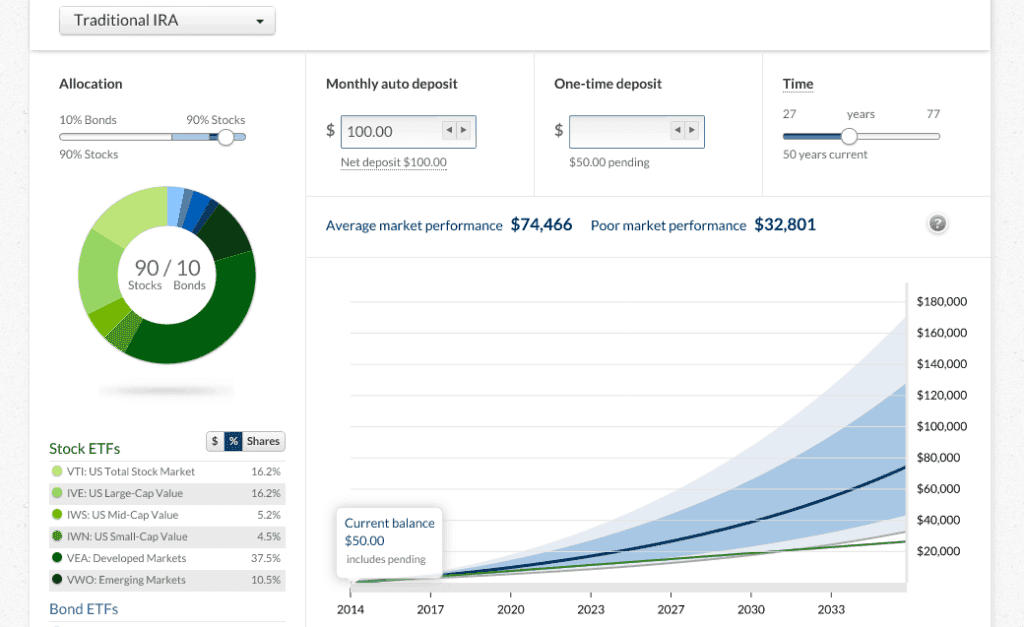

Your goals and risk tolerance, which Betterment learns from its questions when you open your account, help inform the platform’s algorithms to build your portfolio.

People with very little disposable income use Betterment to get a foot in the door as investors without paying fees to certified financial planners. Others have hundreds of thousands of dollars in their Betterment accounts.

The platform remains popular, in part, because of its simplicity and its low minimum deposit of $10 to invest.

Betterment Fast Facts

|

Minimum Investment |

|

|

Management Fee |

|

|

Accounts |

|

|

Features |

|

Features

Here are some of Betterment’s most notable features:

1. Goals Based Investing

In recent years there has been a shift towards “goals-based” investing, which I like because it helps you save towards something tangible like buying a home, college planning, taking a dream vacation, or retirement.

The Betterment platform also lets you know when you are “on-track” or “off-track” to meet your goals and tells you how much more you should be saving to achieve your goal (based on expected returns) within the time frame you have selected.

2. Auto Deposits

Betterment lets you set up automatic deposits from your linked checking account. Automatic deposits allow you to make investing a routine part of your life, which is an essential key to a successful long-term financial plan.

Since the platform offers high-yield savings and checking accounts, you can house all of your accounts in one place and easily withdraw and deposit funds without racking up fees.

3. Cash Reserve and Checking

The Betterment Cash Reserve high-yield savings account makes it easy to move your money between a Betterment investing and a Betterment savings account. This helps ensure that you’re getting the best return on your money while you pursue your investing goals. This account currently pays 3.75% APY.

And you don’t pay management fees based on your cash reserve balance. Betterment will prompt you, a lot, to move money out of your reserve account and into investments.

Betterment also has a fee-free checking account with a debit card, mobile pay, and paper checks. You can also earn cashback on purchases from thousands of brands.

Open an account today with as little as $1.

4. Financial Advising

If you want one-on-one guidance from a certified financial planner, Betterment offers a Premium plan. It gives you unlimited access to one of Betterment’s CFPs, who can help you set and meet your financial goals and assist you with everything from choosing a crypto portfolio to saving for retirement.

The Premium plan comes with a $100,000 minimum balance across all of your Betterment investments. It also has a 0.15% fee.

5. Custom Portfolios

Betterment has 12 expertly-curated portfolios to choose from, including socially responsible and crypto portfolios:

- Core

- Innovative Technology

- Broad Impact

- Climate Impact

- Social Impact

- Goldman Sachs Smart Beta

- BlackRock Target Income

- Cash Reserve

- Universe

- Sustainable

- Metaverse

- Decentralized Finance

If you’re a more seasoned investor, you may want to opt for a Flexible Portfolio. You can start with the Core Portfolio, adjust your allocations, and access more asset classes, like REITS and high-yield bonds.

6. Tools

Betterment has some handy tools to help you plan your financial future, save, and invest. This includes automated tax tools like tax loss harvesting and tax coordination. There’s also a tax impact preview that shows you what you’ll likely owe in taxes before you make a withdrawal.

You can also use the dashboard to view your net worth, track your savings goals, and move your funds around. Betterment lets you link your accounts from other financial institutions to see all of your finances in one place.

Pricing and Fees

Betterment charges a base rate of $4 per month for its investing accounts. That fee automatically changes to 0.25% of your investment balance when you set up repeat direct deposits of $250 or more, or you have a balance of at least $20,000 across all your Betterment bank and investment accounts.

Betterment’s Premium account charges an additional 0.15% fee for human financial advising services. Betterment also has a 1% trading fee on its crypto portfolios.

You can find lower fees and even some free robo-advisors which have a simpler, more streamlined approach. But a Betterment brokerage account offers a lot.

Neither the checking account nor the cash reserve savings account charges monthly fees.

Getting Started

The signup process is simple and straightforward:

- Open an Account: When you open a Betterment account, you will be asked some questions to determine your investing style and goals and to get an idea about your broader financial life.

- Fund Your Account: You’ll then connect your Betterment account to your checking account and transfer some money into your new account.

- Start Investing: Betterment’s algorithms will invest your money into Exchange-Traded Funds (ETFs). Each ETF share includes pieces of many different stocks, which means you can achieve a more diverse investment portfolio without investing a lot of cash.

Security

Betterment does a lot to secure your personal information and protect you from fraud.

The company uses encryption and stores your data on secured servers. They also have a dedicated security team and use safeguards like app-specific passwords, two-factor authentication, and automatic logouts.

If you prefer, you can also use biometric authentication when you log in from your phone, using your face or fingerprint to log in to to the app instead of a password.

Additionally, the Betterment team monitors all transactions and will alert you if something looks suspicious. You can also notify Betterment of fraudulent activity on your account, and they’ll work quickly to address it.

User Experience

I was a Betterment customer for a year and tested out its app, website, and customer support firsthand. Based on my experience and other customer reviews, I rate Betterment highly for user experience.

The dashboard is intuitive and easy to use. You can easily track and adjust your goals, investments, and accounts and get a clear picture of where you stand.

The app is also sleek and intuitive. It has a 4.5 rating in the Google Play store and a 4.7 rating in the Apple App store.

When it comes to customer support, Betterment has a phone line, email, and a virtual assistant chat box. The website also has a pretty exhaustive FAQ page.

You can get live phone support on Monday through Friday, from 9:00 am to 6:00 pm ET. Customers can also schedule paid advisory sessions, which are complimentary for Premium users.

Pros & Cons

Here’s a closer look at the biggest advantages and disadvantages of Betterment:

Pros:

- Fractional shares: Betterment invests your funds into fractional shares, which some robo-advisors don’t offer. That means you don’t have to miss out on a fund just because a full share is out of your budget or just isn’t available. This gives Betterment one more way to allocate your funds appropriately and keep you on track.

- Simple to use: It is an incredibly user-friendly investing platform. The dashboard, app, and resources on the website make navigating your finances easy. As a robo-advisor, Betterment will handle the ins and outs of investing for you, making it a good fit for new investors.

- Friendly goal-specific investing: Betterment is all about goals-based investing. You can aim for growth, retirement, or other future goals, and the platform will suggest portfolios tailored to your timeline, risk tolerance and goals then invest for you accordingly.

- Low costs: Betterment is a low-cost robo-advisor with a lot to offer. Its management fee is par for the course, and it’s less than you’d pay for an actual advisor to manage your investments. Betterment also utlizes low-cost ETFs with minimal fees.

Cons:

- Might be too simple for experienced investors: If you’re a seasoned investor who wants a hands-on experience, you may want to look elsewhere. While I was happy with the user experience and my investments’ performance with Betterment, I wanted to trade actively and access more complex investment tools.

- Limited customer service hours: Betterment is known for offering excellent customer service, but its live service is limited to business hours on Monday through Friday, which is a drawback worth considering. That being said, you can schedule advisory sessions with a Betterment CFP.

My Experience with Betterment

I used Betterment for a year and was happy with the results. I recommend the service for any beginner or intermediate investor because you don’t have to make a significant financial commitment to invest.

Before Deciding to Invest

Before deciding to invest, I spent time researching a number of the best robo advisors, which have grown significantly in popularity over the past few years and include Personal Capital and Wealthfront.

Initial Investment

I initially invested $1,000 with Betterment. After the first three months, I was impressed enough to invest another $50,000.

While investing with Betterment, I found myself checking my investments a lot just because I liked using the app’s unlimited access and seeing my money grow.

But be careful checking too often! It is hard to log in to your account and see that you have lost money when the stock market is down for the day and not be tempted to pull out your money. Just don’t do it!

My Conclusion

New investors don’t always have a reliable sense of risk levels. If you’ve invested in the emerging markets sector, for example, and your portfolio took a big hit, you might be tempted to move toward a more bond-oriented asset allocation.

But millennials have more time to absorb volatility. We are still better off investing over the long term, and there is a strong chance that if you are investing over a 10+ year time horizon your investments in a low-cost index fund-driven portfolio will give you positive returns and help to grow your money.

Betterment offers precisely this kind of investment option for a low cost and without requiring you to become an expert.

I closed my account after a year because I like having a hands-on approach to balancing my portfolio. If I didn’t have time to balance my portfolio and compare ETFs, which I buy directly from Vanguard, I probably would have kept my Betterment account active.

Frequently Asked Questions

Here are some frequently asked questions from readers.

Can you take your money out of Betterment?

Yes, your money flows both ways with Betterment. Your linked bank account can deposit and receive funds from your Betterment account. This process works a lot like making a transfer between two banks. Expect to wait 4 to 5 business days before the transfer finalizes, and your money becomes available in checking.

Betterment will not charge any fees for withdrawals. But withdrawing invested money requires Betterment to sell some, or all, of your investments, and this process could have tax consequences for you.

The good news: Betterment will sell your investments in a way that minimizes your tax loss.

Is Betterment a good investment?

Betterment isn’t an investment strategy in and of itself — it’s just a way to connect you with the market just like any other broker. Its algorithms assume the role of a broker, connecting you with the market but without requiring the fees and commissions a human broker charges.

The platform puts your money into quality ETFs provided by Vanguard, and it chooses ETFs based on the guidelines and goals you share with the system. It’s still not a thorough substitute for a CFP who can discuss the nuances of your portfolio with you. But there’s a low bar for admission and you can learn on your own time.

What does Betterment invest in?

Based on your answers to its initial questions, Betterment will recommend an asset allocation mix between stock and bond ETFs based on your age, tolerance for risk, and goals. Betterment offers ETFs from 12 asset classes.

Although Betterment recommends a ratio to meet your goals most effectively, you can change the ratio of your asset allocation.

How trustworthy is Betterment?

Betterment is a trustworthy investment company with FINRA membership and SIPC insurance. Your account will be protected up to $500,000 by the SIPC, which works a lot like the FDIC to safeguard your bank account balances.

SIPC insurance protects the money in your Betterment cash reserve account in case something went wrong and they could no longer guarantee your deposits. But the platform has a solid track record and has shown no signs of instability.

How could Betterment be better?

Betterment uses Modern Portfolio Theory to guide its algorithms. Investors who’d like a more nuanced approach or more direct control of their portfolios may want a human financial advisor. The platform could also add 529 plans for college savers. The platform also lacks direct indexing which some Robo-advisors use to maximize tax-loss harvesting.

Methodology: How We Review Robo-advisors

At Millennial Money, we use several metrics to provide readers with an accurate review and rating of robo-advisors and other online brokerages.

To evaluate investment platforms, we compare them across these standards:

- Investing options

- Features

- Fees

- Security

- User experience

- Customer support

To learn about these platforms, we rely on customer reviews, first-hand testing, extensive research, and consultations with other experts in the industry.

Read 3 comments or add your own

Read Comments