I was able to retire early at the age of 30 using this exact early retirement strategy. While you might be thinking, how can you retire at 30? Well, it’s important to first define what early retirement actually means to you.

What is Early Retirement?

Early retirement is no longer defined as the moment when you stop working forever, it’s simply the moment when you no longer have to work for money. But you can choose to keep working as I do if that’s what you enjoy doing.

There’s a big difference between doing work you love or a job that you could leave if you get tired of it because you have the freedom and flexibility that saving up enough money can give you.

It’s been scientifically proven that working is actually good for you and many people who completely quit working start losing their mental faculties and people who retire early might actually die sooner.

So to me, early retirement means being able to make the shift from work you have to do to work you want to do. The old school idea that when you retire you are done working, is just that, an old school idea.

Now that we’ve got that settled, let me show you how I retired early and how you can too.

Maximizing Your Early Retirement Strategy

A good early retirement strategy is built on maximizing three levers:

- Income – How much money you’re making

- Expenses – How much money you’re spending

- Saving – How much money you’re saving and investing

The first step in building your early retirement strategy, you need to determine your retire early or financial independence (FI) number – the amount of money you need for work to become optional.

This is by no means an exact science, since it’s a blending of how much money you need to live the life you want today and planning for a future “you” that you haven’t yet become.

Just realize, your number will change and should change, as you change. No matter where you are starting from today, it’s likely going to take you 1, 2, 5, 10, 20, maybe 30 years or more to have enough money to walk away. Over the next years, you’ll want, and need, to refine, your walk-away number calculations as the cost of your lifestyle evolves.

7 Steps to Retiring Early

- Figure Up How Much Money You Need to Retire

- Cut Back On Your Three Biggest Expenses

- Increase & Diversify Your Income Streams

- Set Your Savings Goals

- Create a Simple Investing Strategy

- Fast Track Your Early Retirement Plan by Investing More

- Track Your Savings Rate & Net Worth

1. How Much Money Do I Need to Retire?

While this is a hotly debated topic in the early retirement community, based on a series of papers known as the Trinity Studies, you need to save approximately 25-30x your expected annual expenses to have enough money to last you for the rest of your life.

This multiple is based on what’s known as your expected withdrawal rate, which is the percentage of your investment growth that you would be able to withdraw per year to live on. Based on this study (and many others), a safe early retirement withdrawal percentage is between 3%-4% adjusted for inflation (meaning you can also take out an additional 2%-3% per year depending on inflation).

Here’s how to calculate how much money you need to retire early:

First, figure out how much money you are spending each year by tracking your expenses.

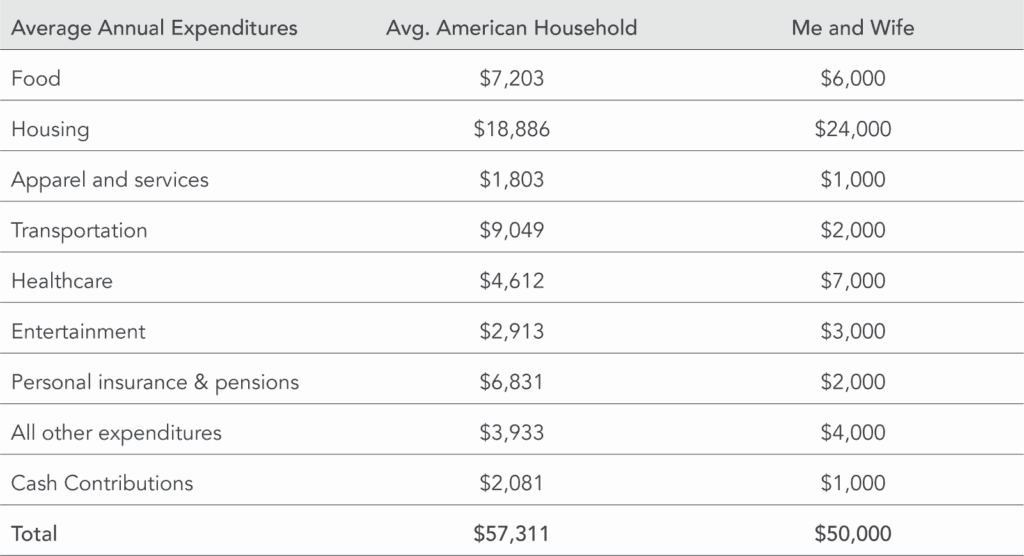

My wife and I spend approximately $50,000 per year, and you can see an approximate breakdown of my expenses by category here:

Using myself as an example, if you spend about $50,000 per year, then you need to have somewhere in the neighborhood of ($50,000 x 25) $1,250,000 to ($50,000 x 30) $1,500,000.

While it’s impossible to account for every variable, where you want to live and whether you want to have kids will have profound impacts on how much money you need to walk away.

If you want a mansion in the Hamptons and an apartment in New York City, you are going to need millions and millions of dollars, which means you will likely need to make some huge tradeoffs in your life while you are trying to save that money.

The less money you can live on, the less you need to retire early.

[Online Tool] Calculate your own current expenses or project your future expenses

2. Cut Back On Your Three Biggest Expenses

What are your three biggest expenses?…

- Housing

- Transportation

- Food

While you can certainly cut back on your small purchases, you’re always going to be able to save the most money where you spend the most money. The average American family spends over 70% of their income on housing, transportation and food.

Here are the most effective ways to cut back on each.

Housing

You should do everything you can to eliminate or even make money on your housing expense. The easiest way to do this is by house hacking, which is a simple strategy where you rent or buy a 2 or 3-bedroom apartment and rent out the extra rooms to offset, completely cover, or even make money on your rent or mortgage.

It’s really easy to do and is the fastest way to increase your savings rate (percentage of your income that you’re saving) and net worth (your assets minus your liabilities).

Transportation

Don’t buy a car if you don’t need one. If you do, always buy a used car. The average American works for a year and a half of their life in order to buy a new car. In most cities in the United States, you can buy a used car that will get you from point A to B safely and is also reliable for under $5,000.

Instead of spending $40K+ on a new car, invest the savings by buying a used car. If you’re commuting to and from work, here are some of our best tips for how to save money commuting.

Food

There are so many ways to save money on food. Make food at home. Buy in bulk. Eat less meat. Calculate your cost per unit when comparison shopping. Whenever you eat out or get your food delivered you’re paying an incredible cost for convenience. Here are some good ways to save money eating out.

Here are another 101 ways to save money.

3. Increase and Diversify Your Income Streams

After you’ve optimized your expenses, the next step is to go out and try to make more money. The more money you make the more money you can save and invest. There are two places you should start – optimizing your full-time job and starting a side hustle.

Back in the day you’d go to school, get a job, work at it for 30-40 years, and peace out into retirement if you made it that far. Your company took care of you with a lifetime pension (free money for the rest of your life!), but now we are left to fend for ourselves. Thankfully it’s never been easier in history to make more money.

Today there are now more tools, strategies, and blueprints for making money. You can learn skills insanely quickly on YouTube in less than a week, you can replicate someone else’s blueprint and map it to your own business, and you can join a community of other people who are working together to make money and build wealth.

Optimize Your 9 to 5

Whether you currently live your full-time job or not, because it’s where you’re making money right now, you should optimize it so you’re making as much money as you can. Negotiate a raise and work remote opportunities so you have more control over your time and more time to make money on the side.

Make sure you’re maximizing all of your employee benefits, including commuter benefits, HSAs, and all retirement investing account opportunities. Here’s a deep dive video into how to optimize your 9 to 5.

Start a Side Hustle

Anyone can go out and make a few hundred extra bucks a week on the side. You make extra money doing anything – mow lawns, walk dogs, shovel snow, babysit, code online, tutor, make deliveries, chauffeur people, flip on eBay, sell a product on Amazon, participate in focus groups, or an infinite number of things.

But not all side hustles are created equal, and some can make you a lot more money than others. The best and worst thing about side hustling is you can literally make money doing anything.

If you are side hustling for someone else, the money you can make will always be limited by the number of hours you have in the day. It’s really tough to get off your 9 to 5 job and hop in a Lyft to drive all night. Sure, people do it and it’s definitely a popular side hustle.

While you might think you are working for yourself, you are actually working for Lyft. Sure, it gives you flexibility and freedom, but no matter how much you drive for Uber or Lyft or deliver for Doordash or Instacart, you’ll always be limited to your own hours. You can’t scale Lyft driving because it’s limited to your own time.

So you need to think about side hustles that you can do and build a business. This doesn’t mean you have to hire your own employers, but you can probably make more money if you do. Profitable side hustling is all about the money/time tradeoff, so you will make a lot more money if you’re the person at the top. This is just one of the many reasons blogging is a great side hustle. To learn how to make money blogging check out my Free 7 Day Blogging Side Hustle Course.

Some side hustles will take a lot more time to get off the ground than others – for example, if you have an amazing idea for a new mobile app, but you don’t know how to code, it’s going to take a lot of time to get that idea off the ground. But mowing lawns in the evenings or on the weekends doesn’t require anything more than the ability to mow lawns.

This doesn’t mean that if you’re busy you can’t find time to side hustle, it just means that you should calibrate the difficulty of your side hustle based on the amount of time you have. I know many families who work side hustle at night after their kids go to bed and some who even bring their kids along on the weekend. They are able to do it, because they schedule their time well and they just really want it.

While you can make money doing pretty much anything, it’s a lot easier to make money doing something you love or at least like – not only are you more likely to stick with it, but it also won’t feel like work.

Video Series

Check out our post on How to Live Without a Job.

4. Set Daily, Weekly, Monthly, and Annual Savings Goals

I break down all of my money goals into daily goals. I still deposit money every day into my investment accounts and track my net worth for free using Personal Capital. Our minds are built to think about today. Our ancestors weren’t able to comprehend years into the future. This is one of the reasons it’s so hard for us to save money.

You’ve probably tried those retirement calculators or have used the retirement projector at Personal Capital. Most of the calculators come out with a number you will need to “retire” based on your inputs and current progression. The numbers are usually big and run into the millions. Who can save $1,272,000 dollars? I was barely able to buy a burrito when I first started.

These numbers are so large, they seem impossible to reach, don’t resonate with us, and actually discourage saving. But, backed by academic research, a lot changes when we start thinking about money in daily increments. If you are nerdy like me and want to go deeper on this topic check out the research of USC professor Daphna Oysterman.

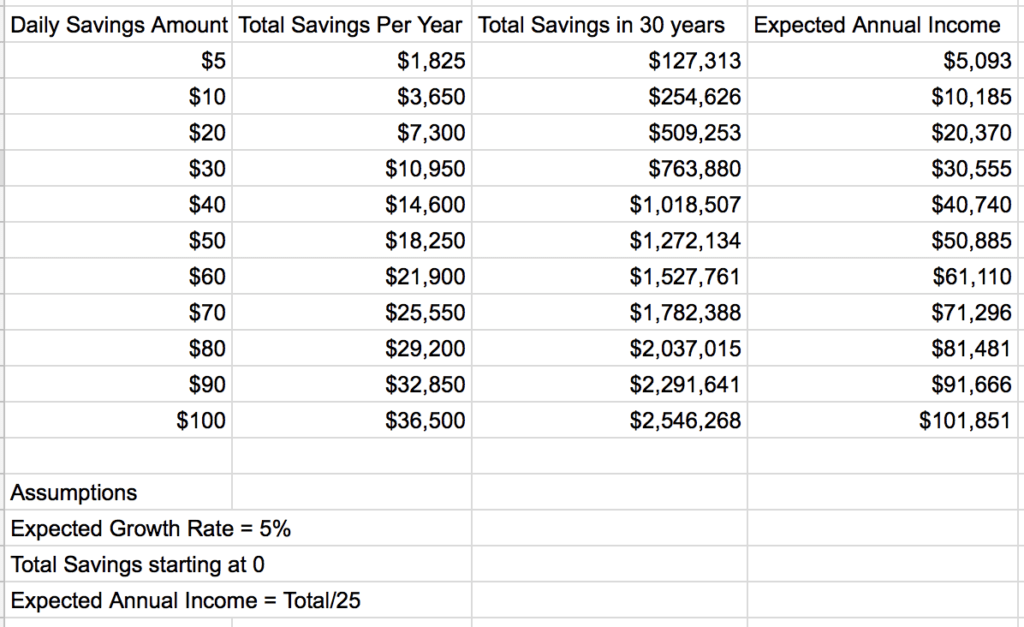

So what should your daily goal be? I did some calculations and determined I needed to try and save approximately $50 a day in order to reach financial independence in 30 years. It can’t be a coincidence that I needed to save a Grant a day!

It’s a simple calculation, and I even created an early retirement calculator that makes it easy to figure out. In order to get to $1,250,000 I needed to save $50 a day and have an expected 5% annual compounding rate (a pretty reasonable expectation over a 30-year period). Thinking about it in annual terms I needed to save $18,250 a year. Max out that 401K!

Then I started really thinking. If I could save even $51 a day then I could fast-track my financial independence. This was a mind-blowing moment for me. Just $1 more per day. I was hooked.

To figure out when you can retire early, check out this early retirement calculator:

Assumptions

5. Create a Simple Investing Strategy

A good early retirement investing strategy should be simple, focused on stocks, bonds, and real estate, and be executed consistently. You should have both a short-term investing (money you’ll need in the next five years) and long-term investing (money you’ll need in 10+ years) strategy.

While you can invest in anything, only invest in what you understand, and stick with asset classes that have performed well historically like stocks, bonds, and real estate. It’s also essential to make sure your money is working as hard as it can for you by investing in a tax-efficient way. This just means that you invest in your accounts the right way.

To learn more about how to invest for early retirement check out my step-by-step posts on best investing strategies and my early retirement investing strategy, as well as my book Financial Freedom, where I’ve outlined a 7-step investing strategy to help anyone retire early.

6. Fast Track Your Early Retirement by Investing More

I started depositing as much money as possible every day into my investment accounts. I downloaded the Vanguard app and literally make deposits every single day directly into my investment accounts. Some days it was only $5, but I rarely missed a day. Then I started a side hustle and put 100% of what I made directly into the same Vanguard account. I barely let deposits clear my bank account. The minute I saw the money in there I put it into an investment account.

I got really stoked when I was able to pass the $ 50-a-day deposit threshold. I started to feel in control. I knew that I was ahead. Every day that I deposited more than $50 I was ahead in my retirement savings.

Then I started trying to make as much money as possible every day so I could invest it. I stopped thinking long-term and thought every day about making that $50 threshold. When I got a bonus or a new client, those were just bonus points. BOOM, right into my investment account.

Do your own calculation – you might need a lot less.

Here is how much you need to save per day to reach your number:

Depositing money into my investment accounts every day felt, and still feels, like a game.

Fifty dollars went from being my daily goal to being my daily minimum. I started depositing $70, then $80, then $100 dollars a day. Then as my side hustles started really taking off I started depositing $500+ a day. Every check I got I put as much in as I could that day, but still kept my daily $50 deposit goal. Then I put $5,000 in a day, then $20,000 and the rest is history.

Using this early retirement hack I was able to reduce my 30-year saving plan down to just 5 years and reach financial independence!

I still do this to this day. Now I automate most of it and simply have the money pulled out of my account and put into Vanguard. My current minimum threshold is $200/day.

But you can start at any level that is comfortable for you. There are a ton of ways you can take this idea and run with it. Try depositing $5/day to start and then increase it $1/week. Trust me you probably aren’t going to miss that extra dollar.

There are a ton of apps you can use like Acorn and Digit to do this for you, but good old-fashioned manual depositing via your investment app (Betterment, Vanguard, Personal Capital, or any others) all make it super easy to deposit.

Personally, I use a combination of both automated and manual investments, since automation is my base and then I supplement it manually.

7. Track Your Savings Rate and Net-Worth

It’s not about how much money you make, it’s about how much money you keep and invest. You want the $1 you make to be worth $5, $10, or $20 in the future. This is how you amplify your time. The two most important numbers to track your early retirement strategy – are your savings rate and your net worth.

Savings Rate

Your savings is the percentage of your income that you’re saving either before or after taxes in all of your accounts (retirement, savings, etc.). There is a direct correlation between your savings rate and the years it will take you to retire early. The savings rate math is simple. No matter how much money you’re making, here’s how long you have to work to save 1 year of living expenses.

Working Years To Save 1 Year of Living Expenses Depending on Savings Rates:

- 10% savings rate: 9 years of work (1-0.1)/0.1

- 25% savings rate: 3 years of work (1-0.25)/0.25

- 50% savings rate: 1 year of work (1-0.5)/0.5

- 75% savings rate: 1/3 of a year of work(1-0.75)/0.75

As you can see the higher your savings rate the faster you’ll be able to retire early. Calculate your savings rate using our savings rate calculator.

Net-Worth

While your income, your savings rate, your investment returns, your debt to income ratio, and all those other numbers are important when optimizing your money, the single most important metric that you should be tracking is your net worth.

Your net-worth measures how much money you are worth by subtracting your liabilities (debt/what you owe) from your assets (what you own that has value, your cash, and investments). It doesn’t matter how much money you make if you spend it all.

Calculate your net worth using our net-worth calculator and monitor your net worth using the powerful free net-worth tracker Personal Capital.

You Can Retire Early Too!

The more you invest every day, the faster you will retire early. If it means that much to you, you’ll make time for it. Every $10 you invest today, could help you reach early retirement days, weeks, or maybe even months sooner in the future. Imagine how much time making that extra investment is buying you in the future time.

Now that you’ve learned how to retire early, you need to pay attention to the mechanics and make decisions that minimize taxes, minimize fees, and invest consistently in the right accounts the right way, so you can reach early retirement as quickly as possible.

To learn more about how to retire early and the exact steps I took to retire at 30 check out my book Financial Freedom: A Proven Path to All The Money You Will Ever Need.

Read 79 comments or add your own

Read Comments