It wasn’t very long ago that I was living at home with my parents with two dollars in my bank account. I was like a lot of my Millennial friends – trying to simply make ends meet and get on with starting my own life.

I also didn’t know anything about saving money or investing. I hadn’t taken any personal finance classes, read any investing books, and surely didn’t learn anything about managing money in high school or college.

The only real thing I knew about money was that not having any sucks. I was tired of living paycheck to paycheck and having my everyday thoughts dominated by whether or not I could afford to live the life I wanted. I knew I had a lot to learn before becoming a millennial millionaire.

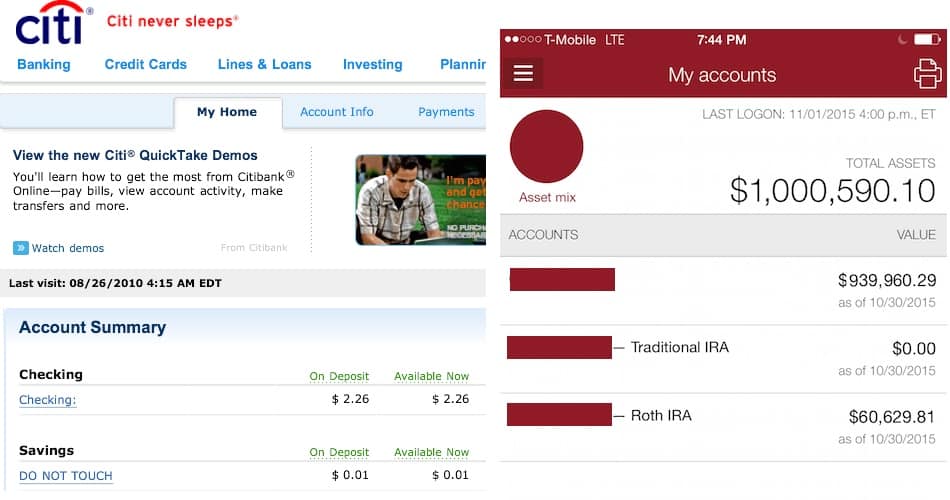

So over the past 5 years, I have spent what is likely an unhealthy amount of time reading about money management, investing, and wealth-building strategies. I have also reached out to industry experts, writers, and money managers. Through this process not only have a learned a ton, but I have also used what I’ve learned to increase my own net worth over the past 5 years from $2.26 to over $1 million.

Looking back I have thought long and hard about how I made this happen and settled on the following ten essential steps and guidelines that I believe were instrumental in helping me to reach this goal. None of these are groundbreaking ideas, but when you put them together they form a simple process where the sum is greater than its parts. I can’t guarantee that you will have the same results, but if you follow even just a few of these steps you are likely going to be much better off financially than you are today.

How to become a Millennial Millionaire

1. Get paid what you are worth

The number one thing that will dictate your future earning potential and get you to $1 million the fastest is how much money you are being paid today. Unfortunately, you probably aren’t being paid what you are worth. A vast majority of the people I know just simply aren’t making enough money to be able to accumulate $1 million within the next 10-20 years. The math just doesn’t work.

Just take your annual salary after taxes and multiply it by 10 and see what the number is – this is why your salary is so important. Here is an unfortunate simple reality that is impacting what you are being paid – the most expensive cost of most companies is their employee’s salaries, so most companies are naturally going to pay you as little as possible to keep you happy. This is how they maximize profit.

Check out my “how to get a raise” guide on how to hack your boss and get a raise. One of my readers just increased in base salary by $7,500 by using the tips in my guide. It’s worth your time.

Do a quick check and see what you are making for others in your role. If you are making less than print out those numbers and take it to your boss and/or HR department immediately and ask to be paid the market rate for your position. This should at least help you get a $5,000 – $15,000 salary bump (which will significantly increase your longer term income potential). Most people don’t get paid what they are worth because they simply don’t ask. Don’t make that mistake.

So what if you are getting paid the market rate and still want to make more money? Find a higher paying career track. Do your research and if you are unhappy with what you see as your future earning potential – pivot and learn new skills, or pick a path or role that will give you more compensation.

For example, maybe you are a Junior Graphic designer making $40,000/year, but if you learned more about the fundamentals of “creative thinking” you could shift into a newly designed “Chief Creative Officer” at an up and coming company and double your salary with your next role. Don’t get stuck early in your career – a simple piece of advice is focus on learning skills and not just trying to get the most senior job titles. At the end of the day your future earning potential is based on what you are being paid today and the value you can create tomorrow.

NEXT STEPS:

- Read my “how to get a raise” guide

- Check your salary against others who have a similar role

- Take that information to your boss or human resource department

- Evaluate more profitable career tracks that relate to your interests

- Focus on acquiring skills, not just job titles

2. Save an insane amount of money

Now that you have asked for more money at your job and are getting paid what you are worth, now you need to start really saving. There are tons of ways to build wealth, but almost all of them require that you have some amount of money to invest. It is a simple, but profound fact that in order to build wealth you need to be making as much money as possible on your money. Because you can only make so much money at any career, investing is truly the key to wealth.

Once I figured this out I made it my number one goal to save and invest as much money as possible. To make this happen I literally overnight started saving 50% of my income – a simple tip: talk to your HR company and have them start depositing at least 20% of your income directly into an investment account before you even see it. This is 20% of your income AFTER contributing to your 401k. I have mine automatically deposited directly into my Vanguard investment account and the money then gets automatically invested into a mixture of index funds.

This is a 100% automated process where I don’t see the money and I don’t miss it. This was a huge mindset shift for me – I started paying myself first and saving as much money as possible. It’s amazing to see how fast your money grows when you start investing it and start making money on your money.

NEXT STEPS:

- Save at least 20% of your after tax paycheck before buying anything

- Set up an automated investing process – make it automatic and leave it alone

- Put the money you save (after you have built an emergency fund) directly into proven investments like index funds and let them compound over time

3. Find a side hustle and invest the profits

Okay, so you are now maximizing your earning potential and saving as much money as you can from your salary. The next step is finding ways to make even more money and invest it. If your goal to build wealth you need to master the side hustle and make money other ways than just your full-time job. This can really be anything, including driving for Uber, consulting, building websites, or start a blog (my personal favorite!).

One thing that I do – I INVEST 100% of the money I make through my side hustles, literally 100% and I have been doing so for the past 5 years. Whether it is $100 I get from participating in a market research study or $10,000 I get for building someone’s website – it all goes directly into my investment account. I do this because the future value of this money will be exponentially greater than spending it today. One tool I like to use is the future value calculator, where you can plug in any amount of money you are planning to spend today and see the future value of this money. Check it out:

I literally have 2 or 3 side hustles going on at any given time and put all of the money directly into Vanguard Index Funds to compound over time. Once you find a great side gig, you will be tempted to spend that money in your everyday life as your bank account grows – but I strongly recommend you think of your side hustle as a key to building wealth (over the long term) instead of just being rich today. Just master the simple rules for investing and you the extra $200+ a week you end up making will turn into tens, if not hundreds of thousands of dollars over the next 10 years. This is about setting yourself up for the future.

NEXT STEPS:

- Find a side hustle – there are literally millions of ways to make extra money

- Invest 100% of your side hustle money

- If you are tempted to spend the money, first calculate the future value of that money

4. Invest in what you know

So you are making more money, have a side hustle, and are investing the profits. Now you need to figure out how to maximize the return on your investments. While I am a big believer in simple index fund investing – it’s pretty boring to just invest in the full stock market. So I always allocate 20% of my investment capital towards individual company’s products I use and believe in.

One of the things we have as hyper-connected Millennials is a perspective on companies and products that older generations of investors simply don’t have. The stock market tends to favor things that are cool, useful, and essential to our lives. To pick a good stock I analyze what everyone else does and use platforms like Simply Wall Street, but I spend a little more time looking at what my friends and the people around me are doing. To me, this is common sense investing.

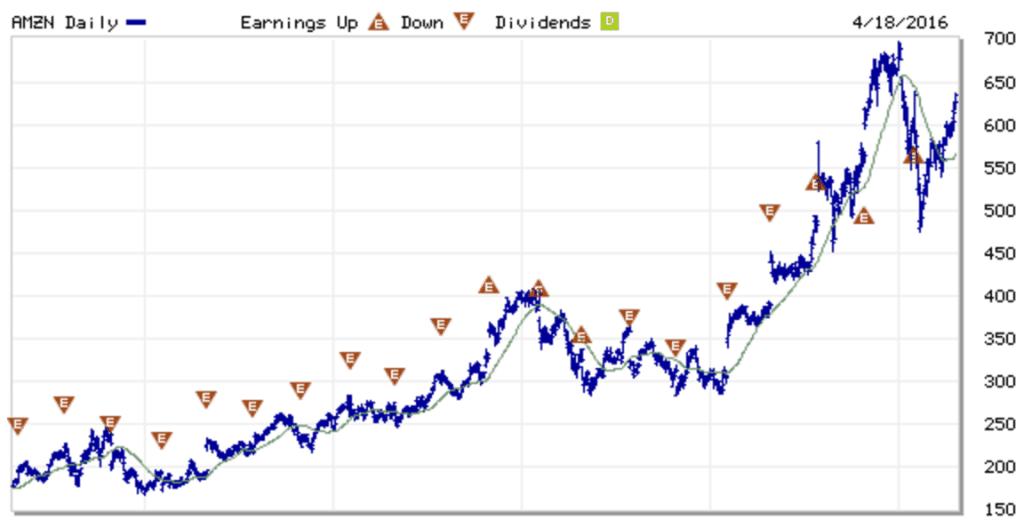

A few simple examples: I first started investing in Apple after getting the first iPhone the first day it came out – I invested $1,000 because I thought it was cool. It’s a pretty similar story with Google – I work in digital marketing and see every day how much money Google makes selling “clicks” and this isn’t likely to slow down anytime soon. Finally with Amazon – I think Amazon might literally take over the world.

Seriously – people today are buying everything from toothpaste to $50,000 watches online. It’s not hard to imagine a day when we will no longer need physical stores and Amazon is leading the e-commerce train. This strategy has generated significant investment returns for me over the past 5 years. My small investment in Amazon alone has generated over $100,000 in profit – all because I believed in their company and decided to click a button.

NEXT STEPS:

- Look at the products you use and consume every day then research the fundamentals of those companies so you can learn more about their investment potential.

- Take a small portion of your investments and put them directly into a few companies

- Continue to evaluate opportunities as you get exposed to new companies and products

5. Measure your net worth closely

Now that you have set your Millionaire Millennial plan in motion – making, saving, and investing more money, now you need to tracking some data and start optimizing your plan. The most important number in your financial life is your net worth. So what is your net worth? It’s the simple calculation of your assets minus your liabilities. It’s what you are truly worth.

I look at my net worth every day when I wake up in the morning and have my morning coffee using Empower. There are few greater motivations than seeing this number rise over time. No matter where you start from. I have been tracking my net worth for the past 5 years and my first balance was $2.26.

Now I have 5 years of my historical finance data that I can analyze with astounding granularity. At the end of the each year I take a deeper dive into this data and track what I have spent the past year on everything so I can work to improve my spending. In 2012 I discovered that I had spent over $3,000 on Mexican take-out food in one year, which is insane and taught me a lesson.

NEXT STEPS:

- Set-up a Empower, formerly Personal Capital, account and link all of your financial accounts to it – don’t worry it’s as safe to use as your bank and has state of the art encryption

- If one of your accounts isn’t available on Empower (a vast majority are) then make sure you manually enter in the information of your asset or liabilities. For example, if you owe your Mom $10,000 then put it in the system as a debt/liability

- Get in the habit of looking at Empower every day – while this might be hard at first, it likely will turn into a huge motivator as you work to increase your net worth

Read 32 comments or add your own

Read Comments