Investing is a major step in your financial life, one that can feel intimidating when you’re just getting started. With the right strategies in place, investing can be an invaluable tool that helps you reach your financial goals.

Read on to learn how to start investing in a few simple steps.

7 Steps to Start Investing

Here are 7 proven steps to follow if you’re ready to start investing:

- Decide How Much You Can Invest

- Open a Tax-Advantaged Investment Account

- Invest Early, Often, and As Much As Possible

- Choose an Investment Strategy

- Make Long and Short-term Investments

- Understand Your Options

- Connect with a Financial Advisor

1. Decide How Much You Can Invest

First, you need to figure out how much you can invest from each paycheck, whether you invest $10 or invest $1,000.

The percentage of your income that you invest is your savings rate. The higher your savings rate is, the faster you’ll be able to reach early retirement. There’s a direct correlation between your savings rate and the number of years it will take you to retire.

According to millennial spending statistics, the average millennial savings rate is 9.8%. If you can increase that to 20%, you can retire in 25 years or less, Increase it to 50%, and you could retire in 15 years or less.

Bottom line: The higher your savings rate is, the faster you’ll reach financial freedom. Start with 10% of your salary (if you’re able), then try to increase that amount by 1% every 30 days.

2. Open Tax-Advantaged Investment Accounts

Taxes are one of the biggest drains on investment returns, so you should aim to minimize your taxes as much as possible.

For most new investors, the number one goal is to invest as much money as possible into tax-advantaged accounts where it can grow tax-free over a long period of time.

There are two types of tax-advantaged accounts you need to know about – 401Ks and IRAs (individual retirement accounts).

The 2026 contribution limit for 401(k)s is $24,500 and the limit for IRAs is $7,500 if you’re younger than 50. Max out these accounts before investing in anything else.

If you work at a company that offers a 401K plan, invest as much as you can up to the maximum. You won’t be taxed on the money that you put in, but you are taxed when you withdraw money from your 401K.

Most companies offer an employee match, which is essentially an employer contribution that matches your own contribution up to a certain percentage of your income (3%-5% is average). This is essentially free money. At a minimum, aim to invest enough to get the match.

3. Invest Early and Often

Albert Einstein called compounding interest “the most powerful force in the universe” and “the greatest mathematical discovery of all time.”

The more time you have, the more opportunity your money has to grow due to compounding interest.

Here’s a simple illustration of how compounding works – the more you invest and the sooner you do it, the faster your money can grow.

A lot of people keep all their money in a savings account because they’re afraid of losing it in the stock market, but the reality is that over any 10+ year period in history, the stock market is likely going to yield positive returns if you invest simply in a stock market index fund.

It’s wise to store an emergency fund somewhere secure like a high-yield savings account. But once you’ve done that, investing is the surest way to build wealth.

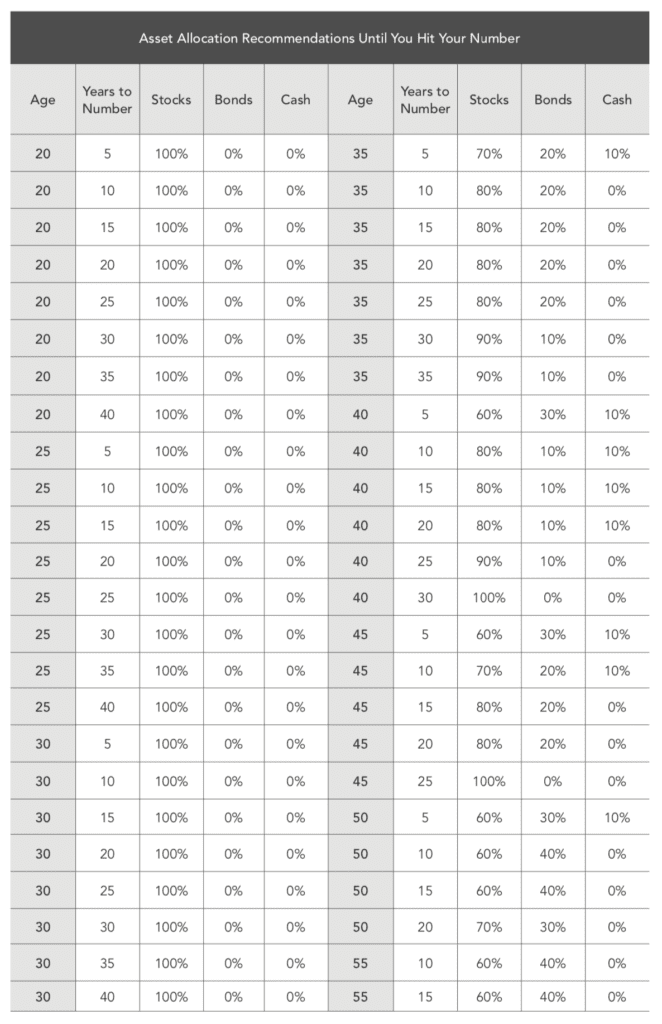

4. Choose an Investment Strategy

There are several investment strategies, and each one has its benefits. The best investment strategies for you to implement depend on your risk tolerance and asset allocation.

I typically recommend that new 401K investors select a model portfolio based on the level of risk they’re comfortable taking.

This is known as your asset allocation, which is the percentage of stocks and bonds you have in your investment portfolio.

If you’re under the age of 35 and starting to invest in a 401K, it could be best to invest in an aggressive growth portfolio, which is heavily weighted in stocks.

The typical asset allocation that makes sense for a millennial is around 90% stocks/10% bonds. Once you hit 35 or 40, it’s best to adjust this allocation to 80% stocks/10% bonds.

While an aggressive portfolio will naturally fluctuate and has more volatility, this is nothing to get scared about when you’re saving for the long term. Over a 10+ year investing horizon, you can make more money investing in stocks than bonds.

Learn More:

5. Make Long and Short-Term Investments

It’s crucial to balance short-term investing with long-term investing strategies. Here are some pointers for each.

Short Term Investments (5 years or sooner)

If you need any of your money in the next 5 years for a purchase like a car, downpayment, or college tuition, you shouldn’t risk losing any of it.

Put your short-term savings in an online savings account with high-interest rates, a CD account, or a money market account (MMA).

Long-Term Investments (5+ years into the future)

Your long-term investments are funds you won’t need to access for at least 10 years, which will include your retirement funds.

There are several types of accounts for retirement savings. Employer retirement accounts primarily include 401(k), 403(b), and 457(b) accounts.

Non-employer retirement accounts, known as IRAs (individual retirement accounts), include the Traditional IRA, Roth IRA, SEP-IRA, and the Solo 401(k).

A Roth IRA is the best retirement plan for young investors, with significant tax advantages over time.

There are a lot of great places to open an IRA or a Roth IRA. My two favorites are Betterment and Ally Invest because of their high-quality low-cost investment options.

If you’re investing for a long-term goal other than retirement, you can also open a brokerage account, which allows you to make penalty-free withdrawals at any age. You may also want to open an account to invest in once you max out your retirement accounts.

6. Understand Your Investment Options

Before you start investing, it’s important to educate yourself on the types of investment options you have to choose from. This will help you make informed decisions and minimize risk.

Here’s a quick overview of the main types of assets you can invest in:

- Stocks: Stocks represent ownership in a company. When you buy stocks, you become a shareholder and have the potential to earn profits through dividends and capital appreciation. Some brokerages let you buy fractional shares of company stocks. Just remember that stocks can be volatile and carry a higher risk.

- Bonds: Bonds are debt securities issued by governments, municipalities, and corporations. When you buy a bond, you are essentially lending money to the bond issuer in exchange for regular interest payments and the return of the principal amount at maturity. Bonds tend to be less risky than stocks.

- Mutual Funds: Mutual funds combine investors’ money to invest in a professionally managed portfolio of diversified securities, such as stocks, bonds, and other assets.

- Exchange-Traded Funds (ETFs): ETFs are like mutual funds, but they’re traded on stock exchanges similarly to individual stocks. They offer diversification and can be more tax-efficient than mutual funds. ETFs are popular for their lower costs and flexibility.

- Real Estate: Investing in real estate involves purchasing properties for rental income or capital appreciation. Real estate can provide a steady stream of income and potential tax advantages. However, it requires careful research and management.

- Commodities: Commodities include physical goods like gold, oil, and agricultural products. Investors can buy and sell commodities through futures contracts or ETFs. They can serve as a hedge against inflation and help diversify your investment portfolio.

- Options and Futures: Options and futures are derivative instruments that give investors the right to buy or sell an asset at a predetermined price in the future. They can be complex and carry higher risks.

- Cryptocurrencies: Cryptocurrencies like Bitcoin and Ethereum have gained popularity as a digital form of currency. Just note that investing in cryptocurrencies can be highly volatile and speculative.

Remember, each investment option has its own risks and potential rewards. It’s important to diversify your investments to spread the risk and consider your financial goals and risk tolerance when choosing your investment options.

7. Connect with a Financial Advisor

Working with a financial advisor can improve your personal finances overall and help you reach your investment goals.

A financial advisor will assess your financial goals, risk tolerance, and time horizon to create a personalized investment plan that aligns with your needs.

J.P. Morgan is one of our favorite financial advisors for new investors, with three flexible investing services.

You can use the robo-advisor to invest in expertly curated and automatically managed funds or try your hand at Self-Directed Investing with unlimited commission-free trades on stocks, ETFs, mutual funds, and options.

INVESTMENT AND INSURANCE PRODUCTS ARE: NOT A DEPOSIT • NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUEFor more personalized service, you can tap into J.P. Morgan Personal Advisors. The service gives you access to a team of financial advisors who develop a tailored financial plan, pair you with the right investment products, and provide ongoing investment advice.

INVESTMENT AND INSURANCE PRODUCTS ARE: NOT A DEPOSIT • NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUEWhether you choose J.P. Morgan or another financial planner or adviser, make sure to work with a fiduciary who is legally bound to act in your best interest when it comes to the financial advice they offer and the investment decisions they make.

Start Investing Today

A lot of people don’t invest because they think of it as gambling, but the truth is, you control the amount of risk that you take.

You can invest in literally anything you expect to increase in value over time, from art, cryptocurrencies, and tax liens to secure investments in stocks, bonds, and real estate.

If you’re hesitant to take a big risk, you can choose an investment vehicle with a proven track record and plenty of research surrounding it.

If you follow the guidelines above, you’ll be well on your way to building wealth and making work optional. To learn more about how to invest check out my bestselling book Financial Freedom: A Proven Path to All The Money You Will Ever Need.

How to Start Investing: According to Your Current Financials

Have a certain amount of money you are looking to start investing with? See our detailed guides on how to best move forward:

- How to Invest with Very Little Money

- How to Invest $100

- How to Invest $500

- How to Invest $1,000

- How to Invest $5,000

- How to Invest $10,000

- How to Invest $20,000

- How to Invest $30,000

- How to Invest $50,000

- How to Invest $100,000

- How to Invest $200,000

- How to Invest $250,000

- How to Invest $300,000

- How to Invest $500,000

- How to Invest a Million Dollars

- How to Start Investing in College

- How to Invest and Make Money DAILY

Read 4 comments or add your own

Read Comments