Frugality has always been a deep part of my life, but this year I ran from frugality with reckless abandon. And I’m officially adding “Losing Frugality” to my list of top millennial money mistakes. I hope you don’t make the same mistake. Seriously. For as much as I write about personal finance and have made a lot of smart decisions about money the past 5+ years, this past year I lost the frugality that has been one of the core drivers of building my net-worth. And my financial future has suffered because of it.

Since this year I’ve always been a very frugal person. I inherited my frugality from my father, who is one of the most frugal people I’ve met in my life. We both share the rare distinction of only buying 1 or 2 new pairs of pants every year.

My father grew up with very little and has passed on that frugality to me through many life lessons over the years. I also credit my frugality (and automated savings), as the two greatest factors in me achieving financial independence and becoming a millennial millionaire by the age of 30.

But, this past year something changed. My frugality disappeared. Instead of buying $12 bottles wine, I started buying $50+ bottles (yes they taste better but I only bought $50+ bottles).

I stopped cooking and ordered $75 in takeout on a Wednesday night. I stopped flying coach and upgraded to business class on most flights (sometimes with miles sometimes paying extra). Instead of booking a normal hotel room or Airbnb, I opted for the rooms with a view.

What happened to packing my lunch at home, limiting my grocery trips to less than $50, buying my shoes on eBay, only buying my jeans on sale, and the frugality that helped me become financially independent?

How did I seriously spend $12,000 on a weekend in Napa Valley? Even though I could technically “afford it,” my spending and savings rate has gotten way out of whack and I’ve abandoned the frugality that’s gotten me where I am today.

Sure, I’ve had a really fun year that’s included traveling all over the world, an oceanside wedding in California, and bought some cool stuff. But it’s gotten way out of hand. I’ve lost my way. I’ve lost the frugality that was not only better for me, but better for the earth too.

It used to be the “take what you need an leave the rest” frugality that made me happy. Not buying the best. It’s also frugality that I know is essential to helping me continue to increase my net worth over the coming decades. It’s scary looking into the future as I see my spending habits growing significantly and getting out of control.

For a deeper perspective checkout the Millennial Money podcast episode on lifestyle inflation and the paradox of frugality.

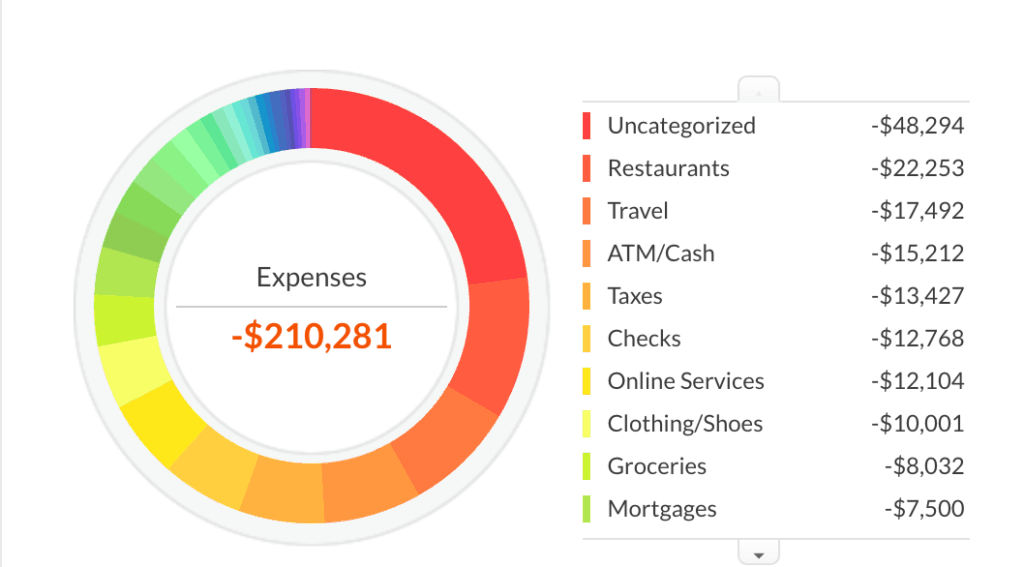

I’ve never spent more money in my life than in 2016 – with my spending rate increasing an astronomical 134% over last year, and peaking at over $210,000! Yeah, I just pulled these numbers from Personal Capital last week and couldn’t believe the totals. I knew that I was spending a lot of money, but got out of the habit of checking my spending/saving balance regularly. I literally have a deep pit in my stomach writing this. But I’m learning from it and hope that radical transparency will help me improve next year.

How I spent over $210,000 in one year

So what happened? It’s actually a pretty simple story. I spent way too much money. My balance between spending on saving was seriously out of whack. Looking at my Personal Capital account, it’s easy to see where the money went. Just look below. I spent an insane amount on takeout restaurants, traveling, new furniture, gifts, clothing, business services, groceries, and a wedding.

As my income has continued to increase so has my spending, so much so that I stopped paying attention to the day to day transactions and making smart purchasing decisions. Yes, my investments, including my Millennial Money portfolio are growing and generating a strong return, but I’m not building on my principle balances like I did for the past 5+ years that are essential to building my financial future.

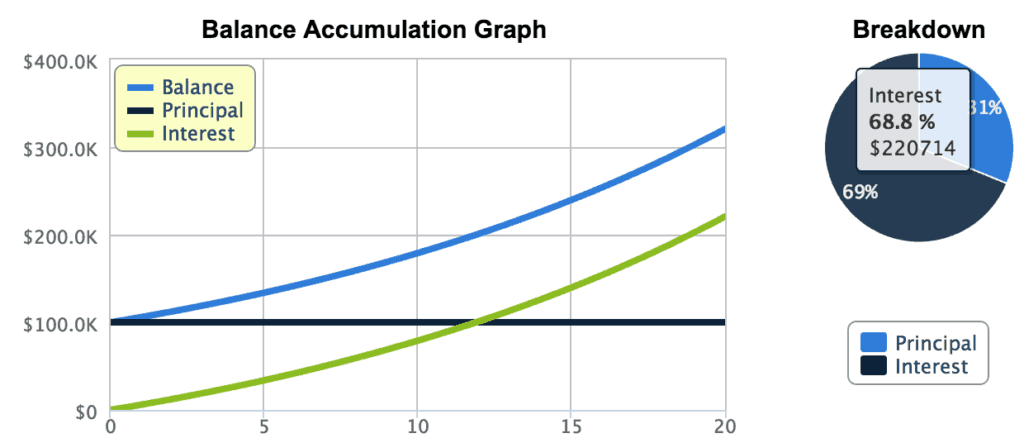

I am left not only thinking about the $210,000 but also about the future value of the money that I spent. Realistically when I look back at my itemized spending I see how I could have pretty easily saved $100,000 if I was following the habits I used previously in building my net-worth. Hypothetically let’s just take a look at the future value of saving $100,000 of what I spent.

The Return on My Lost $100,000 over the next 20 years

A simple future value calculation (with an expected rate of return of 6%) shows that I would have $302,713.55 in 20 years just investing that $100,000 principle and not adding a single dollar more. That’s a ton of future earnings that I’ve lost and won’t ever get back.

A Return to Frugality

But I can only move forward. So how can I return to frugality? It starts with changing my habits again. And changing my habits starts with each decision I choose to make. So yesterday I made the choice, and each day need to make the choice to recommit to frugality. It comes down to every purchase decision.

I was recently inspired by my Millennial Money Minutes podcast co-host Matt who shared in his 5 Frugality Lessons that he used to think that frugality was about saving, but frugality is really about spending wisely. I couldn’t agree more.

I was also inspired by Coach Carson’s quote about frugality in his How Frugality Buys Freedom post: “Every dollar you spend is really a choice between the object you purchase and increased life options. Frugality, or deliberately spending less, is actually a conscious choice to purchase more freedom.” This reminded me of my first Millennial Money post Money is Freedom and is an important reminder.

Finally, I returned to a Mr. Money Mustache post on frugality that inspired me a few years ago, where he shares “Learning to separate “happiness” from “spending money” is the quickest and most reliable way to a better life. The side-effect of this is that your life will become much less expensive and you will, therefore, become much wealthier very quickly.”

Capital One Shopping compensates us when you sign up for Capital One Shopping using the links we provide.

My Breakthrough Moment

Last week I had a small breakthrough moment. I’ve needed a new computer bag for a while. One to take my computer to my office and to take on the road. I travel a ton for my business – often taking a trip every few weeks. Since I spend an unhealthy amount of time in airports, anything I can do to make my trip more efficient or more comfortable adds up to a better travel experience.

I’ve wanted a Tumi computer bag that could easily slide onto my roller bag for a long time, but my current computer bag hadn’t worn out until this year. So I started looking at new bags a few months ago.

Earlier in the year, I would have bought a new bag without thinking, but this past week I just couldn’t push myself to pay $350+ for a computer bag. I just couldn’t do it. I could feel a return to frugality.

So I set up an eBay alert and started hunting for a deal. Then I got an alert for the exact model I was looking for (one that retails for $429) on sale for $39 on eBay. I put in a bid and won the bag (with no other bidders). The bag arrived just like new. It’s a simple purchase, but it felt great to get a deal. It’s a small decision I hope to repeat daily when faced with the choice to spend or save.

Since that purchase, I haven’t ordered take out food. I bought an $8 bottle of wine last night. And I booked a $49/night Airbnb for an upcoming trip (the best deal I could find).

I’ve returned to frugality. I feel like myself again.

What do you do to stay frugal?

Read 24 comments or add your own

Read Comments