Financial literacy is something everyone needs. Many of the decisions we make strongly depend on our understanding of money.

Financial literacy is lacking in the US, however. Many people enter adulthood without a firm understanding. Yet, most of us deal with money every day. Whether paying bills, applying for a credit card, or investing, we’re constantly exposed to money.

Twenty-three states currently have laws or regulations requiring high school students to take at least a semester-long personal finance course either currently or by 2028, which is a step in the right direction, but America has a long way to go.

Top Financial Literacy Statistics

Here are some of the top financial literacy statistics to consider.

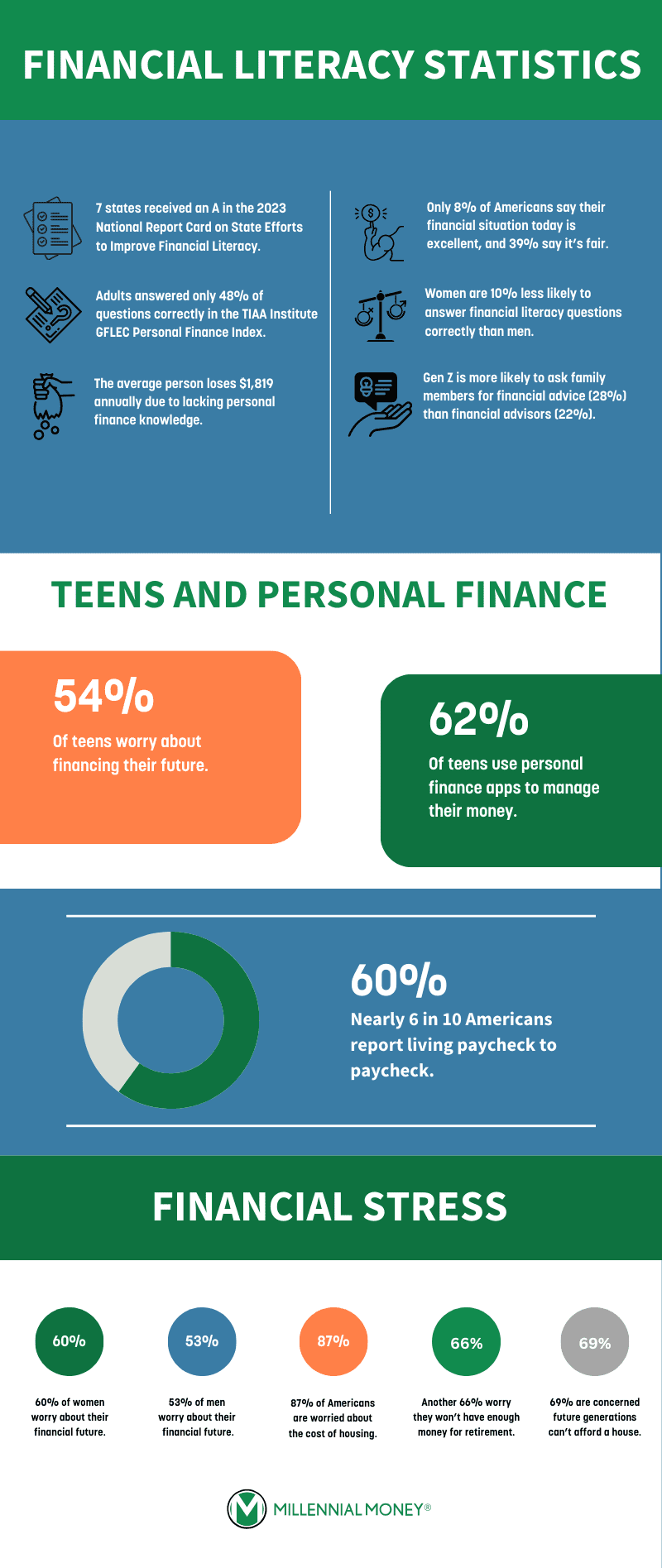

- The 2023 National Report Card on State Efforts to Improve Financial Literacy gave only 7 states an ‘A.’ This means schools in these states must provide a stand-alone personal finance course versus combining the education into other course material.

- According to the TIAA Institute-GFLEC Personal Finance Index, adults answered only 48% of 23 questions correctly in 2023. This is a decrease from 50% in 2017.

- The average person loses $1,819 annually due to lacking personal finance knowledge.

- Only 8% of Americans say their financial situation today is excellent, compared to 12% in 2021, and 39% say it’s fair.

Women are 10% less likely to answer financial questions correctly than men.

In the TIAA Institute-FFLEC Personal Finance Index, 43% of women answered questions correctly versus 53% of men. In addition, only 10% of women got 22 – 28 questions right out of 28, but 23% of men answered them right.

60% of women and 53% of men worry about their financial future.

With low levels of financial literacy, high inflation rates, and depleted savings accounts, millions of people lie awake at night worrying about their financial future, including 60% of women and 53% of men. 35% of those surveyed lose sleep over their finances and 63% of parents with young children worry they won’t be able to make ends meet.

Gen Z is more likely to ask family members for financial advice, than financial advisors.

28% of Gen Z is more likely to ask financial questions of their family versus 22% who seek advice from a financial advisor. This is compared to 19% of millennials, 12% of Gen X, and 8% of Boomers who would ask their family members for financial advice.

54% of teens worry about financing their futures.

Sixty nine percent of teens say that increasing post-high school education costs changed their mind about school, and 39% say they would feel better equipped if they had a better understanding of how student loans worked.

62% of teens use personal finance apps to manage their money.

This number is up from 48% in 2019, and 38% of teens still prefer to use cash to manage their finances, and 57% of teens say their parents give them cash when providing them with money versus using electronic forms of payment.

Almost 60% of Americans live paycheck-to-paycheck.

As of August 2023, 60% of Americans live paycheck-to-paycheck and 19% struggle to cover their monthly bills. In the 60% of Americans living paycheck-to-paycheck, 45% were high-income earners.

81% of households are fully banked.

19% of households use nonbank forms of payment such as money orders, rent-to-own services and pawn shops. Leaving 81% of households fully banked and able to manage their finances using traditional banking products.

58% of Americans don’t have an emergency fund.

Fifty eight percent of Americans don’t have a designated emergency fund. In addition, 49% of Americans are incapable of handling a $1,000 financial emergency, despite 93% of Americans experiencing such emergency at least once.

87% of Americans are worried about the cost of housing.

Fifty five percent of Americans claim they cannot afford housing prices right now, and 87% are worried about the cost. The worry passes down to children and grandchildren with 69% of people surveyed concerned future generations cannot afford to purchase a house.

78% of households are surprised when they overdraft their checking accounts.

Despite many banks doing away with overdraft fees on checking accounts, 78% of households are still surprised when they spend more than they have, proving that more needs to be done about financial literacy in our country.

15% of households claim at least one family member was a victim of financial fraud.

Fifteen percent of households state that at least one member of their family was tricked into sending money or giving access to their financial accounts, which can likely be due to the lack of financial literacy in the country.

66% of Americans worry they won’t have enough money for retirement.

With rising costs, high inflation rates, and the financial crisis during the pandemic, 66% of Americans worry about retirement. Because of this 41% of Americans surveyed stopped putting money into their retirement plans and 32% withdrew retirement savings to cover the higher cost of living.

America has $1.08 trillion in credit card debt.

America as a whole has $1.08 trillion in credit card debt and 56% of active credit cards carry a balance.

The Future Of Financial Literacy

Recent developments show increased importance of teaching kids about money. However, an important question is whether this trend will accelerate.

Of course, trends are always difficult to predict. But growing levels of debt suggest more financial education may be necessary.

As it stands today, many states have a long way to go. Legislation constantly changes and hopefully more states get on board with the need to improve our financial literacy statistics.

Doing so could help consumers be more informed and able to make decisions. But will the current financial literacy trend continue? Only time will tell.

No comments yet. Add your own