Everybody has a unique financial situation. Your location, lifestyle, job, and family size greatly affect your monthly expenses.

As such, it can be challenging to see how you stack up against others—especially when it comes to monthly budgeting.

Comparing your monthly expenses to the average American can help you understand where your money is going and if you’re on track.

This article explores the average monthly expenses for one person. We’ll also examine the most significant factors contributing to your monthly spending.

How Much an Average American Spends

According to a recent Consumer Expenditure Survey from the U.S. Bureau of Labor Statistics (BLS), the average American household spends about $6,080 each month. Annually, that amounts to about $73,000.

By far, housing is the most expensive cost for most people, with an average cost of around $2,077 a month (around 26% of a typical family’s income).

Transportation is the average person’s next highest expense at an average monthly cost of around $1,024 (roughly 13% of the average household income).

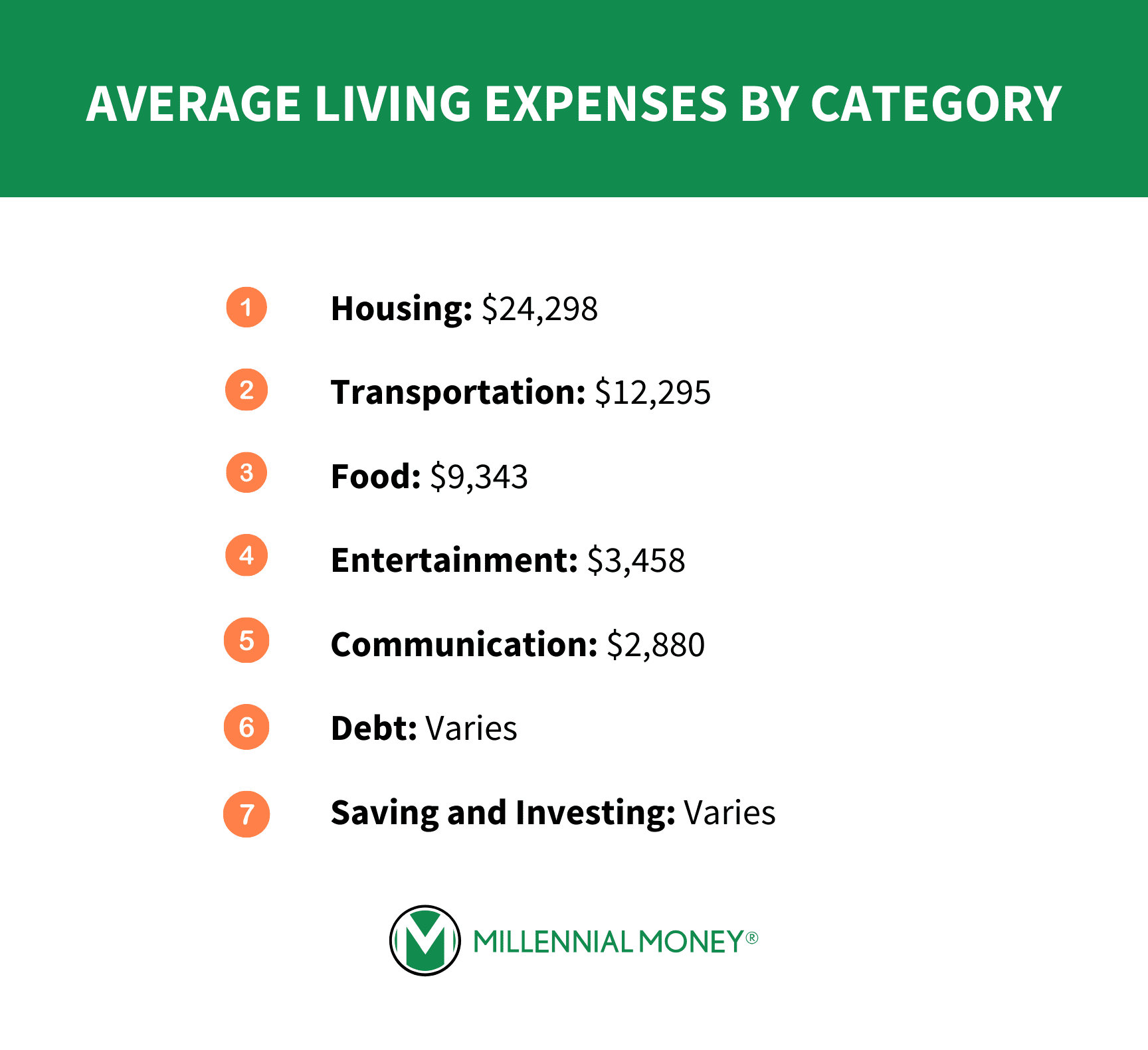

Average Living Expenses by Category

Let’s take a closer look at these top spending categories.

- Housing Costs: $24,298

- Food Costs: $9,343

- Transportation Costs: $12,295

- Communication Costs: $2,880

- Entertainment Costs: $3,458

- Debt Costs: Varies

- Saving and Investing: Varies

1. Housing Costs: $24,298

Unless you have the luxury of living in an inherited home or with your parents, you must pay for housing. It’s a basic necessity, and chances are it’s your highest monthly cost.

It’s important to be selective about where you live to keep your costs down. Ideally, there should be a progression where your first apartment sets you up to move to a nicer apartment. After that, you may buy a condo or apartment and eventually buy a house.

If you overspend on your first apartment, you could fall into debt trying to make monthly payments, setting you back years financially.

At the same time, housing is important. You should feel safe, comfortable, and happy where you live. So in some cases, you may feel justified in spending more money on housing, especially if you have a decent job that pays well.

The general rule of thumb is that housing shouldn’t take up more than 30% of your gross earnings or what you make before taxes. This includes rent or mortgage payments, property taxes, homeowners insurance, mortgage insurance (if you can’t afford a 20% down payment), renters insurance, utilities, and maintenance and repairs.

2. Food Costs: $9,343

Food is expensive, but you have to eat to live! Most people typically allocate roughly 10% of their income to their food budget. If you’re spending more than this on food every month, you should reconsider your grocery shopping strategy and look for ways to cut back.

Chances are there are some small things you can do to reduce your food bills. For example, you can use coupons or buy in bulk from a wholesale club like BJ’s, Costco, or Sam’s Club to lower the average cost of food, or you can limit the amount of take-out you order monthly and learn how to stop eating out.

If you shop wisely, you should be able to buy enough food on a budget to last you through the month.

Eat healthily, be smart about ordering out, and your food budget should stay in check.

3. Transportation Costs: $12,295

Regarding transportation, you generally have a bit more say over how much you spend every month.

Many people drive cars that are too expensive, or they simply drive too much. By making small changes to your lifestyle or routine, you can potentially cut back on transportation costs and pump more money back into your savings and investments.

You may not need to buy a car if you live in a city. Use public transportation, buy a bicycle, ride-sharing and carpooling services, or try walking whenever possible.

A recent study shows that the national average commute is more than 52 minutes daily. You may even want to consider finding a job that lets you work from home to eliminate this time and lower your transportation costs.

Either way, you should keep transportation costs at 10% to 15% of your total budget. This includes car payments, insurance, parking, maintenance and repairs, and gas.

If you really want to fast-track your financial freedom, I recommend spending no more than 5% of your monthly income on transportation.

4. Communications Costs: $2,880

If you’re like most people, you depend heavily on communication for everything from work to staying in touch with friends and family.

Communications costs may include high-speed internet, mobile service, and television. You may also need a landline telephone for work.

Most people spend roughly $140 monthly on cell phones and another $100 or so for internet and cable. If you spend more than $240 per month on communications, break down your costs and look for ways to lower your bill. You could be overpaying.

It’s also worth considering additional communications expenses that may affect your budget. For example, you may be paying for cloud services, an Office 365 subscription, or apps. Do a communications audit and ensure you aren’t carelessly throwing money away every month.

5. Entertainment Costs: $3,458

Here’s some bad news: If you’re like the average American household, you are most likely spending too much on entertainment, which is about $288 per month (3.6% of a family’s monthly income).

This is an extra cost you can likely cut back on. If you have Netflix, you may not need Hulu and Prime Video too, for example. It may also be time to cut the cord and stop spending so much on video game equipment.

By capping your entertainment budget and reducing the amount you spend on frivolous fun, you can put yourself many years ahead financially. If you invest and save an extra 5% of your budget—or even just 4%—you will likely add tens of thousands to your net worth over the next ten to twenty years.

6. Debt Costs: Varies by Individual

If you’re in debt, you need to get out of it as soon as possible. Start by checking your credit cards and student loans to figure out how much debt you have. If you have multiple accounts with interest rates averaging 20% or higher, you should treat it as a financial emergency and start making aggressive payments.

How much you put towards debt largely depends on your debt load. If you’re in deep, you may want to put 20% to 25% of your income toward debt.

It may also be a good idea to consider a private loan to pay off your credit cards and consolidate your payments. You may receive a lower interest rate, and it’s easier than paying down multiple cards each month.

Remember, you’ll usually get a better return from paying down high-interest debt instead of putting your money into a high-growth account. There’s little point in saving or investing if you’re losing money each month to debt payments.

Above all else, don’t lose sight of the light at the end of the tunnel. If you’re in debt, you can get out. You just need to make it a financial priority, even if it hurts in the short term.

7. Saving and Investing: Varies by Individual

You must prioritize saving and investing when determining your monthly expenses and setting a budget.

If you’re living paycheck to paycheck, you may not like putting money into the bank for an emergency fund. It’s worth it, even if it means cutting out your entertainment expenses or reducing transportation costs to make it work.

Far too often, young people don’t make saving and investing a priority. As a result, they wind up paying for it in the worst way possible: with time.

Unfortunately, time is the most important factor when planning for the future and growing money. You can never get back lost time for saving and investing. The more you put away for growth today, the better off you’ll be in the long run.

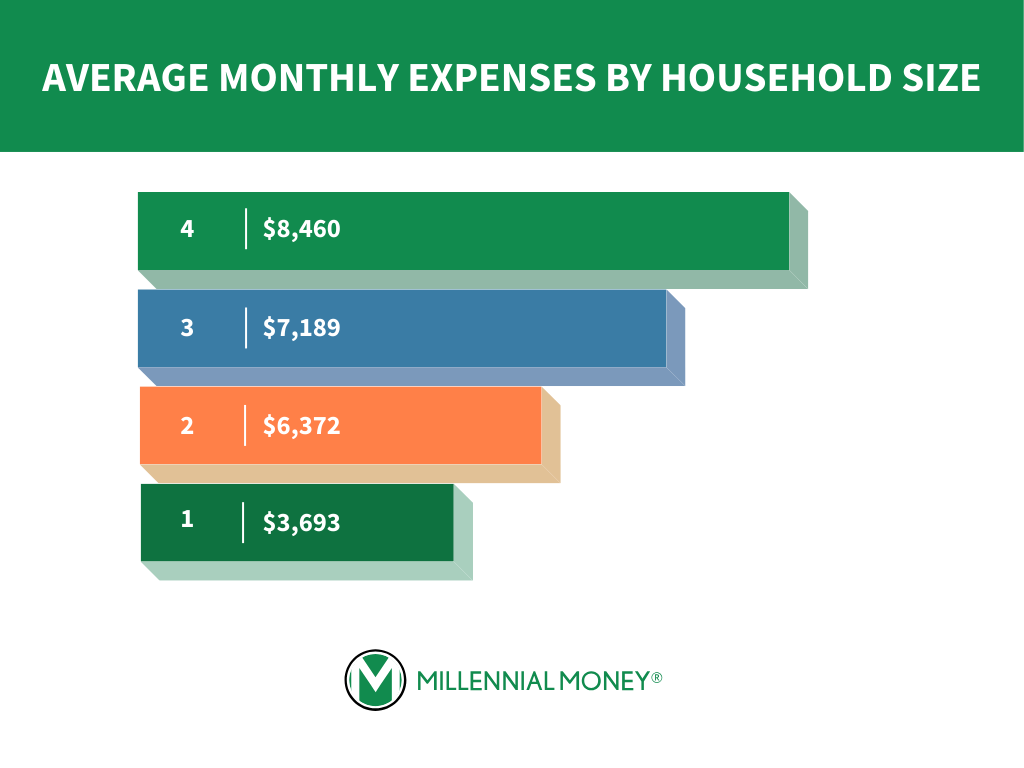

Average Monthly Expenses by Household Size

The data provided by the U.S. The Bureau of Labor and Statistics provides the information as a ‘household,’ but households can mean many things from one person to many, so here’s how average monthly expenses break down by household size.

- Average Monthly Expenses for One Person: The average monthly expenses for a single person annually is $44,312, or $3,693 per month.

- Average Monthly Expenses for Two People: Two people spend an average of $76,468 annually, which is $6,372 per month.

- Average Monthly Expenses for Three People: Three people spend $86,265 per year, or $7,189 a month.

- Average Monthly Expenses for Four People: As you likely expect, monthly expenses for four people is higher, at $8,460 per month, or $101,514 annually.

Average Monthly Spending by Age

The average monthly spending by age may surprise you as the highest spending is during ages 45-54, with an average spending of $91,074.

The age group with the least spending is those under age 25, at $46,359.

It’s not surprising that age groups 45 – 54 spend the most on food annually, spending $11,827 per year, but the 35 – 44 age group is right behind them at $11,023. That’s a considerable difference compared to the overall average of $9,343.

When it comes to housing, the lowest spending occurs under age 25, as that’s before many people are ready to buy a home. People in this age group spend only $16,837 per year. The spending peaks between ages 35 – 54, when most people buy homes and subsequently pay them off, with housing costs averaging $28,975 at ages 35 – 44 and $28,281 at ages 45-54.

At age 65, annual spending drops drastically to $57,818, which is $15,000 less than the average.

How Average Monthly Expenses Changed Year Over Year

Looking at how average monthly expenses change year over year can help you understand a lot about your budget and where your money went.

Housing saw an 8.4% jump in spending from 2021 – 2022, which isn’t surprising given how the housing market performed over that time. Many people moved during the pandemic, upgrading to homes they could comfortably work and attend school in.

Apparel spending saw a 10.9% increase, and food saw a 12.7% increase in spending from 2021 to 2022. Vehicle purchases were one expense that decreased. From 2021 to 2022, these expenses dropped 6.9%, likely because not as many people were commuting and vehicle inventory was so low.

Tips for Controlling Expenses

Consider Using Budgeting Rules

There are several budgeting frameworks you can follow to help allocate money appropriately.

For example, the 50/30/20 rule says you should spend up to 50% of after-tax income on necessities like food and shelter. After that, you can put 20% into savings and debt and 30% into anything else you want.

There is also the 70/30 budget rule, which says you should take your monthly earnings and put 70% into monthly expenses, 10% into savings, 10% into investments, and 10% into donations.

You can modify these rules to fit your lifestyle and unique budgetary requirements. You just need a plan.

Check out some of the best budgeting apps for 2026.

Start a Side Hustle

Work as much as possible when you’re young and save as much as you can. There are so many different side hustles to choose from to supplement the earnings from your full-time job.

You can walk dogs, babysit, paint houses, manage social media, or wait tables. You can also choose to drive for a service like Uber or deliver groceries for a service like Instacart.

The more you make, the easier it is to handle monthly expenses and still meet your savings and investing goals.

Consider Roommates

Living on your own can be rewarding, but it can also be very expensive. When you have roommates, on the other hand, you can split bills evenly, which reduces your monthly expenses and gives you more money to put aside.

If you have a two- or three-bedroom apartment, you may want to consider renting it out and slashing your monthly housing bills. This strategy is called house hacking.

Consider your Location

Living in expensive cities like San Francisco, New York City, and Los Angeles offers many advantages. However, the cost of living in these places is also jaw-droppingly high.

If you’re looking to save money, it may be a good idea to consider moving to an area with a cheaper cost of living or find a job that lets you work from home full-time.

Look for states with little or no income taxes and lower housing and food costs. You may find it easier to get by in a city or town that aligns with your budget.

Frequently Asked Questions

Are childcare costs expensive?

If you’re expecting a child, you must put as much money aside as possible. Kids can typically cost around $1,000 per month or more when factoring in all the care and services they need. At the same time, you also need to factor in putting money aside for their future. It’s a good idea to have at least two income sources to ensure the child is adequately cared for. The last thing you want to do is run short on financing with a kid. Should that happen, you could wind up in a tough situation.

Should I lower my insurance premiums?

It depends on how healthy you are, how much you drive, and how much you make. You probably don’t need an expensive health insurance plan if you’re single and healthy. If you don’t drive much, then you probably don’t need a premium car insurance plan, either.

However, there are risks to lowering your insurance premiums, and it could come back to bite you. Good insurance can really pay off when you need it, even if it means overpaying when you don’t.

Do I need life insurance?

It depends. If you have a family or people who depend on you, you probably should have life insurance. If that describes you, your best bet is to lock it in while you’re young and healthy so that you pay less for premiums. If you wait too long, you could develop a health issue, increasing your premiums.

On the other hand, if you are a single person with no dependents, I would say that life insurance is more of a nice-to-have. Either way, if you are in a position to save lots of money, you may not need it because you can self-insure.

Think of it this way: Let’s say you save over $1,000,000 in investments. You can access these funds at any point during your life, and they get passed down to your loved ones after you pass away. This makes life insurance a little unnecessary. Your life insurance agent would probably disagree with this opinion, though!

The Bottom Line

Now that you know what factors into your monthly budget, it should be obvious that your situation is unique to you and you alone, and only you can control it. A budget is essential whether you’re managing monthly expenses for one person or five.

Create a monthly budget based on your household income and expenses. Stick to it, and you’ll inch closer to long-term financial independence every day.

Sure, it might seem like you can’t control some things, such as where you live and how much you make. But in today’s golden era of remote work and side hustles, you have more power than it may seem. It might even be as simple as knowing how to negotiate a raise.

Don’t be afraid to think outside the box and look for ways to get ahead. You’ll be happy that you did down the road.

No comments yet. Add your own